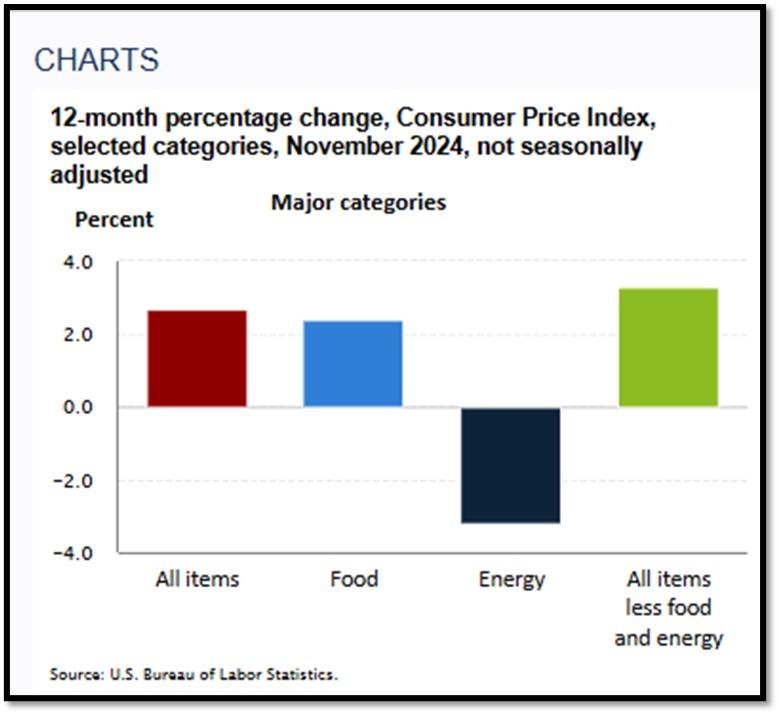

- 1. The U.S. Consumer Price Index (CPI) rose by 0.3% in November, aligning with market expectations and bringing the annual inflation rate to 2.7%.

- 2. (Not Investment Advice) The investment landscape is rapidly evolving, offering a range of opportunities driven by technological advancements, sustainability trends, and emerging global markets.

- **With the current macro-economic backdrop, below are areas we currently favor:

- 3. The healthcare sector is undergoing a profound transformation, driven by shifts in policy, technology, and the evolving needs of patients.

- 4. World Watch

- 5. Quant & Technical Corner

1. The U.S. Consumer Price Index (CPI) rose by 0.3% in November, aligning with market expectations and bringing the annual inflation rate to 2.7%.

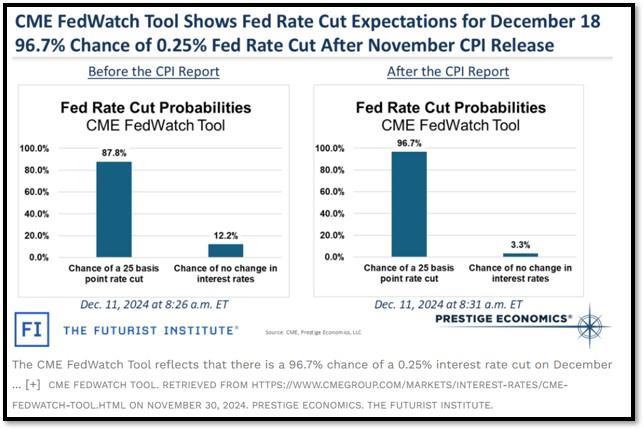

This slight uptick, while above the Federal Reserve’s 2% target, is not anticipated to deter the Fed from implementing a 25 basis point interest rate cut during its December 17-18 meeting. Financial markets have largely priced in this rate reduction, with futures indicating a 98% probability of the cut. This expectation is bolstered by Federal Reserve officials’ recent communications and the overall economic outlook. Despite the modest increase in inflation, the Fed appears focused on supporting economic growth and addressing potential headwinds, such as trade uncertainties and global economic slowdowns. The anticipated rate cut aims to sustain the current economic expansion and maintain favorable financial conditions. See item 5K further below for additional information on the most recent CPI report. REF: BARRON’S, Forbes

2. (Not Investment Advice) The investment landscape is rapidly evolving, offering a range of opportunities driven by technological advancements, sustainability trends, and emerging global markets.

Key areas of growth include artificial intelligence (AI), green energy, healthcare innovations, and infrastructure development. In the technology sector, AI continues to lead with innovations in automation, cybersecurity, and semiconductors. Companies like Nvidia and Google are driving AI adoption across industries. Similarly, the growth of renewable energy and electric vehicles (EVs) presents significant potential. Investments in solar and battery technologies, alongside EV manufacturers and charging infrastructure firms like Tesla and ChargePoint, align with global sustainability goals.

Healthcare is another promising arena, particularly in precision medicine and biotech. Advances in gene therapy and personalized treatments from firms like CRISPR Therapeutics are revolutionizing patient care. Additionally, AI integration in diagnostics and health management enhances efficiency and outcomes. Click onto picture below to access video.

Global infrastructure spending, particularly in the United States, is fueling opportunities in construction, logistics, and smart cities. Companies like Caterpillar and Siemens are poised to benefit from initiatives to modernize energy grids and transportation systems. Meanwhile, emerging markets in Asia and Africa offer growth driven by rising populations, technological adoption, and expanding economies.

**With the current macro-economic backdrop, below are areas we currently favor:

- Fixed Income – Short-term Corporates (Low-Beta)

- Fixed Income – Corporates High Yield as Opportunistic Allocation (Low-Beta)

- Businesses that contribute to and benefit from AI & Automation (Market-Risk)

- Small Cap & Mid Cap Stocks (Market-Risk)

- Utilities (Market-Risk)

- Healthcare & Biotechnology (Market-Risk)

- Gold (Market-Risk)

- Industrials (Market-Risk)

- Asian Equity (Market-Risk)

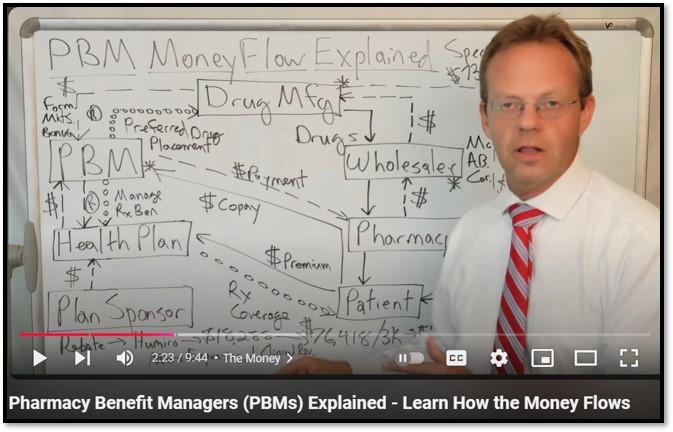

3. The healthcare sector is undergoing a profound transformation, driven by shifts in policy, technology, and the evolving needs of patients.

Central to this shake-up is the expected overhaul of pharmacy benefit managers (PBMs), the billing system, and a gradual transition from a reactive, drug-heavy model to a more proactive, cure-based approach to healthcare. PBMs, which act as intermediaries between drug manufacturers, insurers, and pharmacies, have faced increasing scrutiny due to opaque pricing and profit-driven practices. Reforms are expected to emphasize greater transparency, ensuring that patients and insurers benefit from fair drug pricing. This change is critical as skyrocketing prescription costs have become a barrier to care, and a streamlined PBM system will reduce unnecessary financial burdens on patients.

Another significant development is the modernization of billing systems. Traditional healthcare billing is often complex, inefficient, and prone to errors, leading to administrative waste and patient frustration. Emerging technologies like artificial intelligence and blockchain are streamlining claims processing, improving accuracy, and enhancing cost-efficiency. A simplified billing process will lead to better patient experiences and reduced overhead for healthcare providers.

Perhaps the most transformative shift is the movement away from a reactive, drug-heavy model of treatment to a proactive, cure-based approach. Historically, healthcare has focused on managing symptoms with pharmaceuticals, which, while profitable for manufacturers, often fails to address the root cause of diseases. Advances in precision medicine, gene therapy, and preventative care are redefining this paradigm. Innovations now aim to cure diseases at their source, leveraging genetics, early diagnosis, and personalized treatment plans. This proactive strategy not only improves patient outcomes but also reduces long-term costs associated with chronic disease management. These changes signal a fundamental evolution in healthcare. The restructuring of PBMs, modernized billing systems, and a shift towards proactive cures reflect a collective push for greater transparency, efficiency, and patient-centered care. This transformation promises to make healthcare more equitable, accessible, and effective for all. Click onto picture below to access video. REF: HealthAffairs, Forbes, McKinsey&Co

4. World Watch

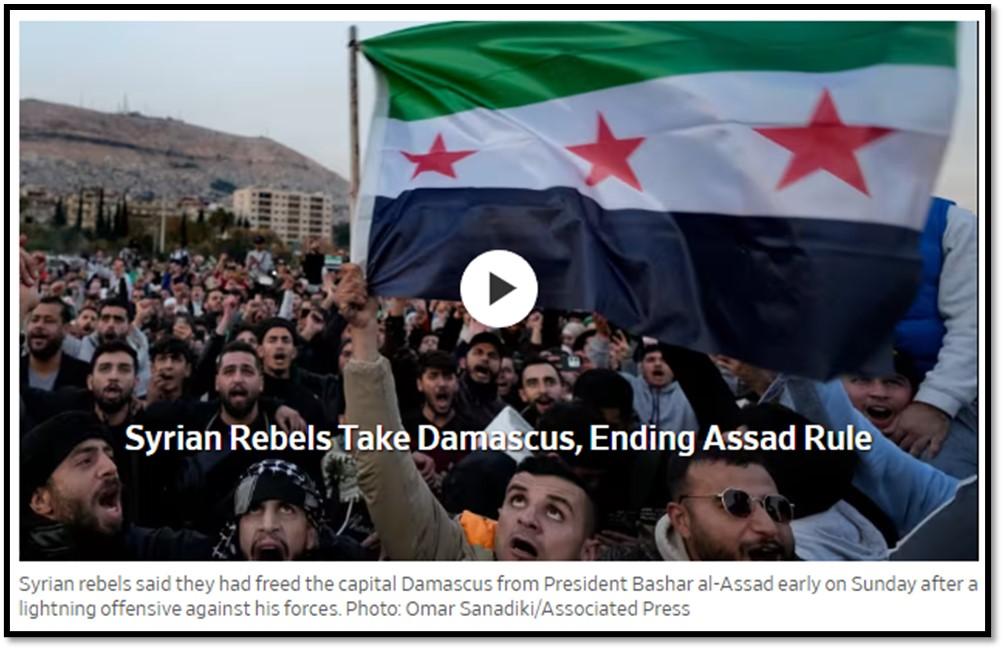

4A. The Fall of Assad and Its Implications for Syria and the Middle East according to The Wall Street Journal. The collapse of Bashar al-Assad’s regime marks a turning point for Syria and the broader Middle East. After decades of Assad family rule, Syrian rebel forces swiftly captured Damascus, forcing Assad to flee to Russia. The weakened Syrian military and years of economic decline accelerated the regime’s downfall. In the aftermath, a transitional government led by Mohammed al-Bashir has been formed, with promises to maintain state institutions and ensure accountability. However, challenges remain, including uniting Syria’s diverse factions and preventing further fragmentation. Regionally, Assad’s fall has weakened Iran, disrupting its strategic influence and supply routes to Hezbollah in Lebanon. Conversely, Turkey has gained influence, reshaping the region’s balance of power. The international community, including the U.S., has cautiously supported the new government, provided it upholds minority rights and renounces extremism. While Assad’s removal brings hope for a more inclusive Syria, the road ahead is uncertain. The nation’s ability to achieve stability will depend on cooperation among domestic and international stakeholders. Click onto pictures below to access insightful videos from WSJ. REF: WSJ

4B. For over half a century, South Korea’s economy has been dominated by family-owned conglomerates known as chaebols. These entities, including giants like Samsung and Hyundai, have wielded substantial influence, often prioritizing familial control over shareholder interests, leading to complex business practices that enrich insiders at the expense of minority investors. The recent political upheaval, marked by President Yoon Suk Yeol’s brief imposition of martial law, has intensified scrutiny of these conglomerates. The political instability has highlighted the urgent need for corporate governance reforms to address the “Korea discount,” a term describing the undervaluation of South Korean stocks due to governance concerns. The government’s “Corporate Value-up Program,” initiated to enhance transparency and shareholder value, has seen limited compliance, with only 12% of companies in the KOSPI market engaging with the initiative. This lackluster participation underscores the challenges in reforming entrenched corporate practices. The political crisis has galvanized both regulators and investors to push for more substantial reforms. The potential ouster of President Yoon has created a window for accelerating these efforts, aiming to dismantle the oligarchic structures that have long stifled economic equity and transparency. Click onto picture below to access video. REF: Bloomberg

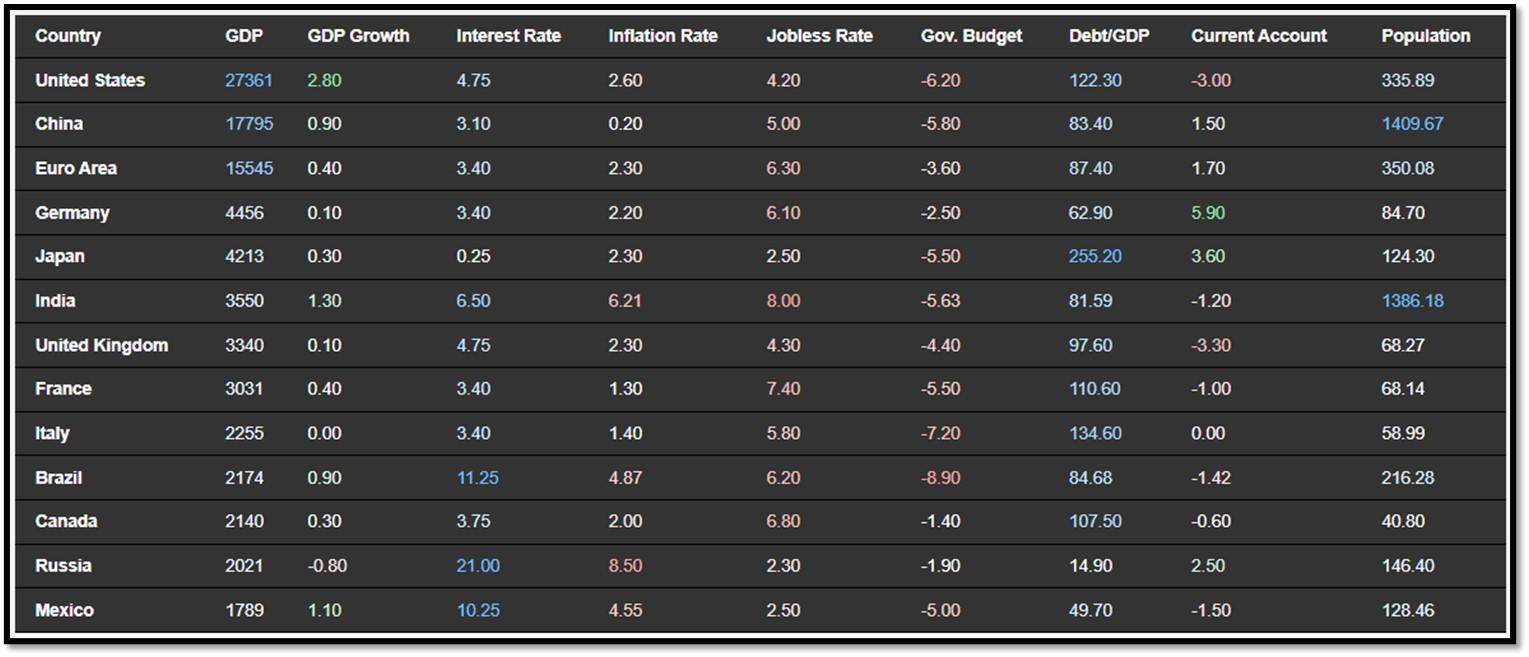

4C. Below is an updated snapshot of the current global state of economy according to TradingEconomics as of 12/10/2024. REF: TradingEconomics

- The unemployment rate in the United States went up to 4.2% in November of 2024 from 4.1% in the prior month, in line with market expectations.

- China’s annual inflation rate unexpectedly eased to 0.2% in November 2024 from 0.3% in the previous month, falling short of market forecasts of 0.5% and marking the lowest figure since June.

- Japan’s GDP expanded by 0.3% quarter-over-quarter in Q3 2024, above flash data and market forecasts of 0.2%.

- Unemployment Rate in India decreased to 8 percent in November from 8.70 percent in October of 2024.

5. Quant & Technical Corner

Below is a selection of quantitative & technical data we monitor on a regular basis to help gauge the overall financial market conditions and the investment environment.

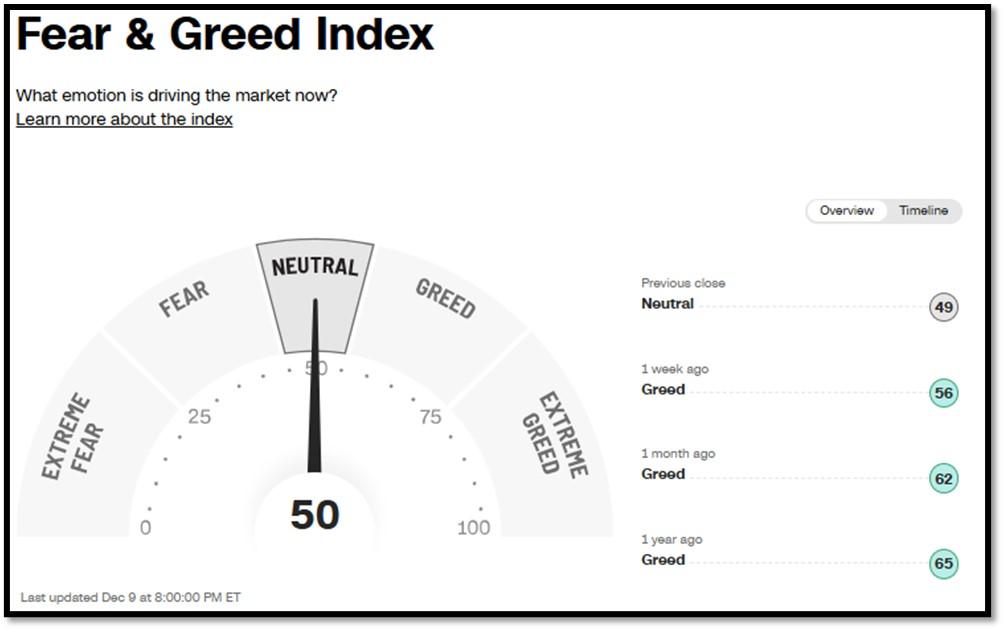

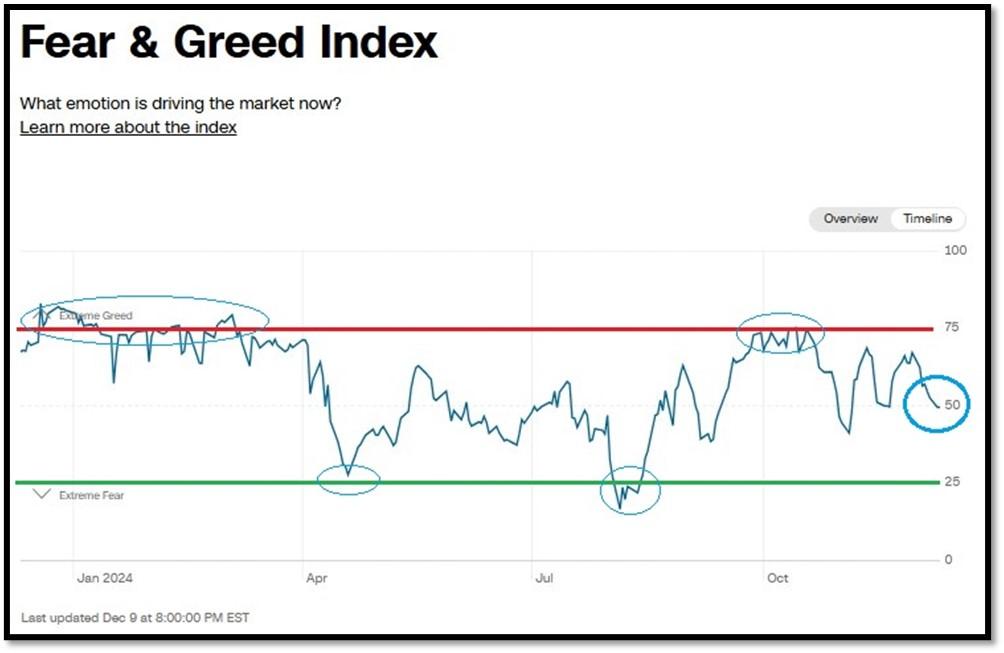

5A. Most recent read on the Fear & Greed Index with data as of 12/9/2024 – 8:00PM-ET is 50 (Neutral). Last week’s data was 56 (Greed) (1-100). CNNMoney’s Fear & Greed index looks at 7 indicators (Stock Price Momentum, Stock Price Strength, Stock Price Breadth, Put and Call Options, Junk Bond Demand, Market Volatility, and Safe Haven Demand). Keep in mind this is a contrarian indicator! REF: Fear&Greed via CNNMoney

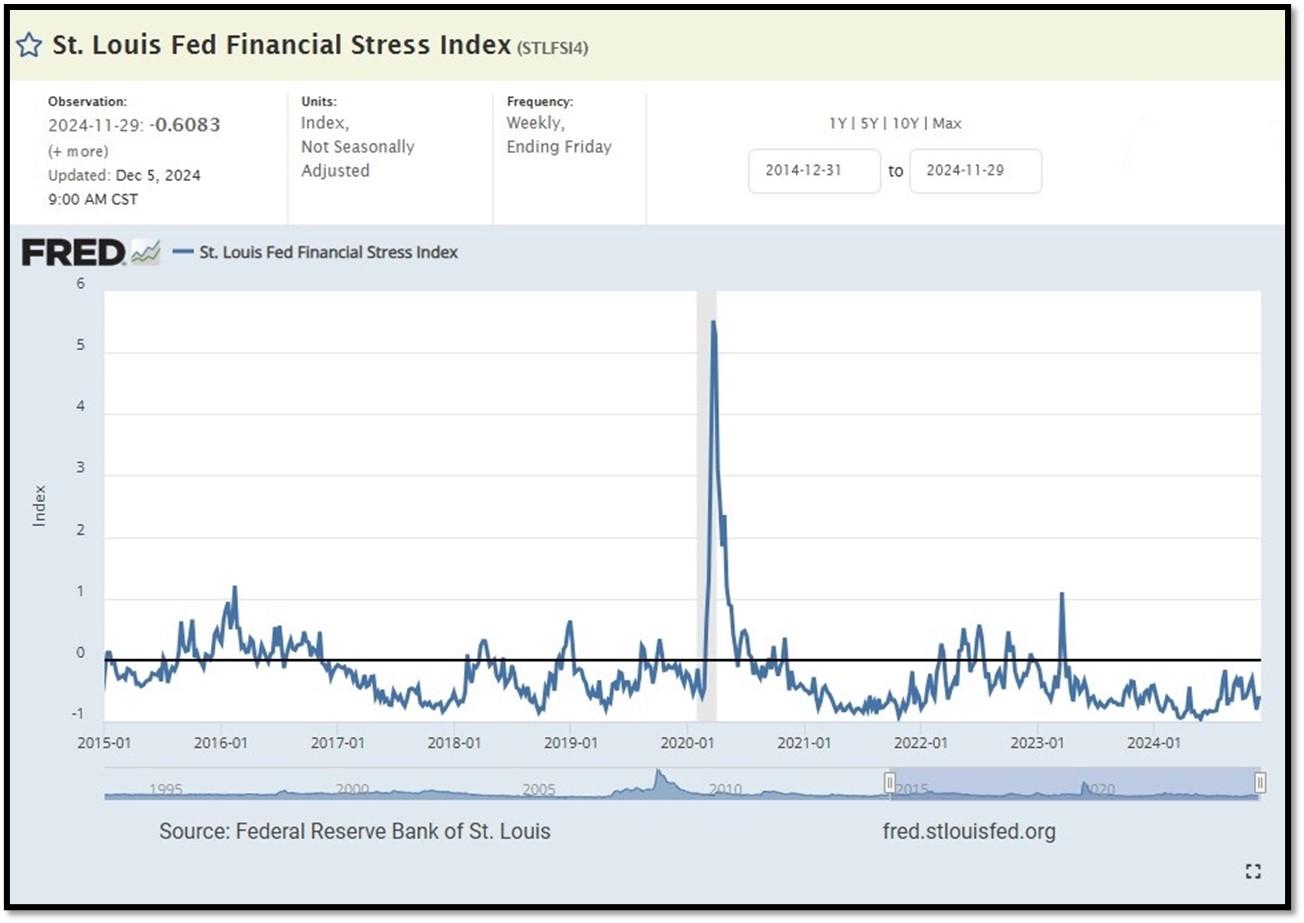

5B. St. Louis Fed Financial Stress Index’s (STLFSI4) most recent read is at –0.6083 as of December 5, 2024. A big spike up from previous readings reflecting the recent turmoil in the banking sector. Previous week’s data was -0.6153. This weekly index is not seasonally adjusted. The STLFSI4 measures the degree of financial stress in the markets and is constructed from 18 weekly data series: seven interest rate series, six yield spreads and five other indicators. Each of these variables captures some aspect of financial stress. Accordingly, as the level of financial stress in the economy changes, the data series are likely to move together. REF: St. Louis Fed

5C. University of Michigan, University of Michigan: Consumer Sentiment for September [UMCSENT] at 70.5, retrieved from FRED, Federal Reserve Bank of St. Louis, October 25, 2024. Back in June 2022, Consumer Sentiment hit a low point going back to April 1980. REF: UofM

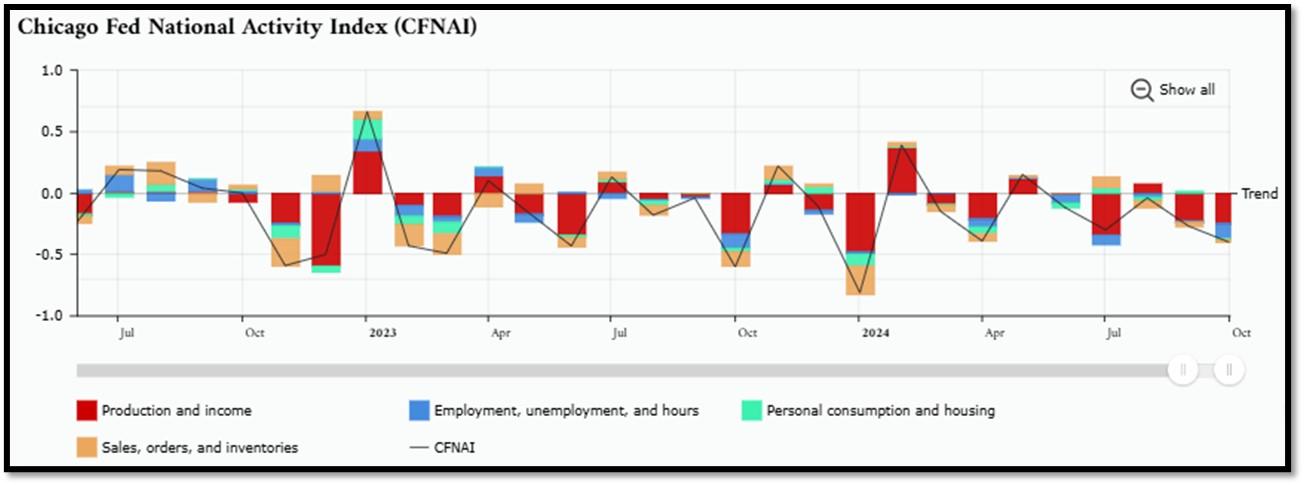

5D. The Chicago Fed National Activity Index (CFNAI) decreased to –0.40 in October from –0.27 in September. Three of the four broad categories of indicators used to construct the index decreased from September, and all four categories made negative contributions in October. The index’s three-month moving average, CFNAI-MA3, decreased to –0.24 in October from –0.21 in September. REF: ChicagoFed, October’s Report

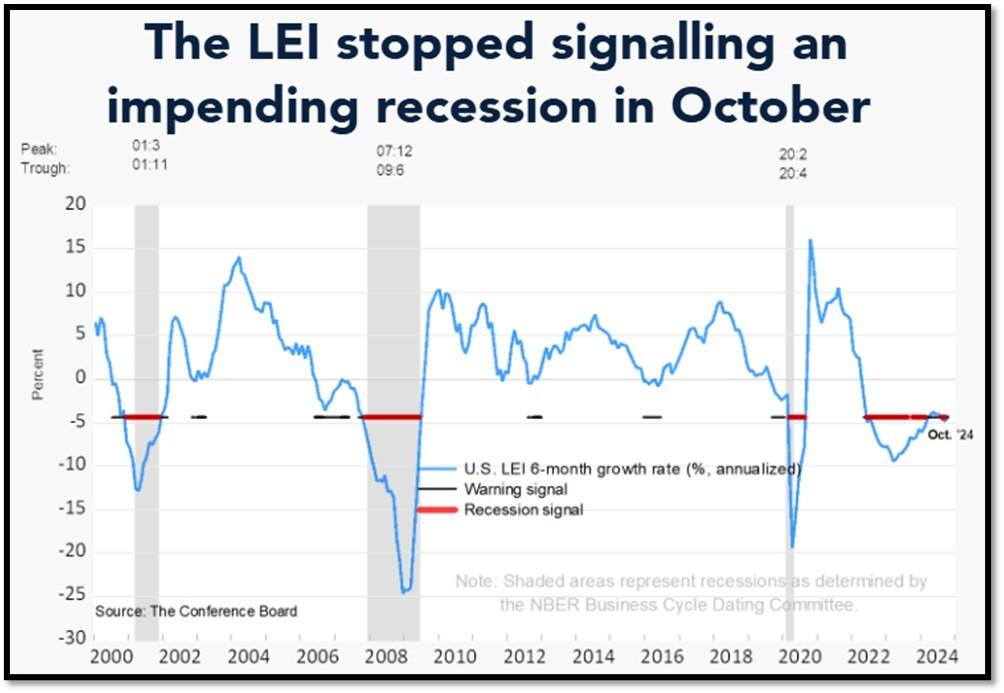

5E. (11/21/2024) The Conference Board Leading Economic Index (LEI) for the US declined by 0.4% in October 2024 to 99.5 (2016=100), following a 0.3% decline in September (revised up from a 0.5% decline). Over the six-month period between April and October 2024, the LEI fell by 2.2%, slightly more than its 2.0% decline over the previous six-month period (October 2023 to April 2024). The composite economic indexes are the key elements in an analytic system designed to signal peaks and troughs in the business cycle. The indexes are constructed to summarize and reveal common turning points in the economy in a clearer and more convincing manner than any individual component. The CEI is highly correlated with real GDP. The LEI is a predictive variable that anticipates (or “leads”) turning points in the business cycle by around 7 months. Shaded areas denote recession periods or economic contractions. The dates above the shaded areas show the chronology of peaks and troughs in the business cycle. The ten components of The Conference Board Leading Economic Index® for the U.S. include: Average weekly hours in manufacturing; Average weekly initial claims for unemployment insurance; Manufacturers’ new orders for consumer goods and materials; ISM® Index of New Orders; Manufacturers’ new orders for nondefense capital goods excluding aircraft orders; Building permits for new private housing units; S&P 500® Index of Stock Prices; Leading Credit Index™; Interest rate spread (10-year Treasury bonds less federal funds rate); Average consumer expectations for business conditions. REF: ConferenceBoard, LEI Report for October (Released on 12/2/2024)

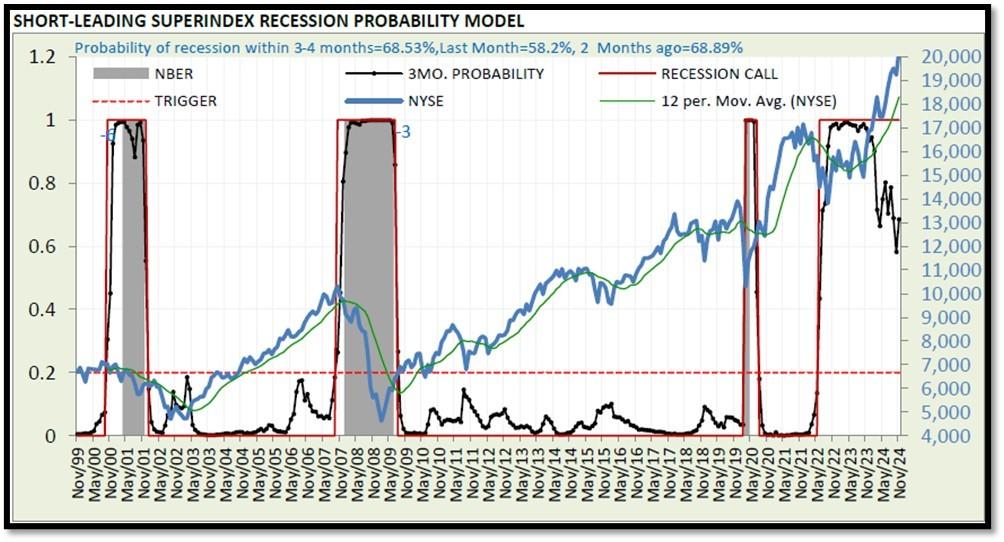

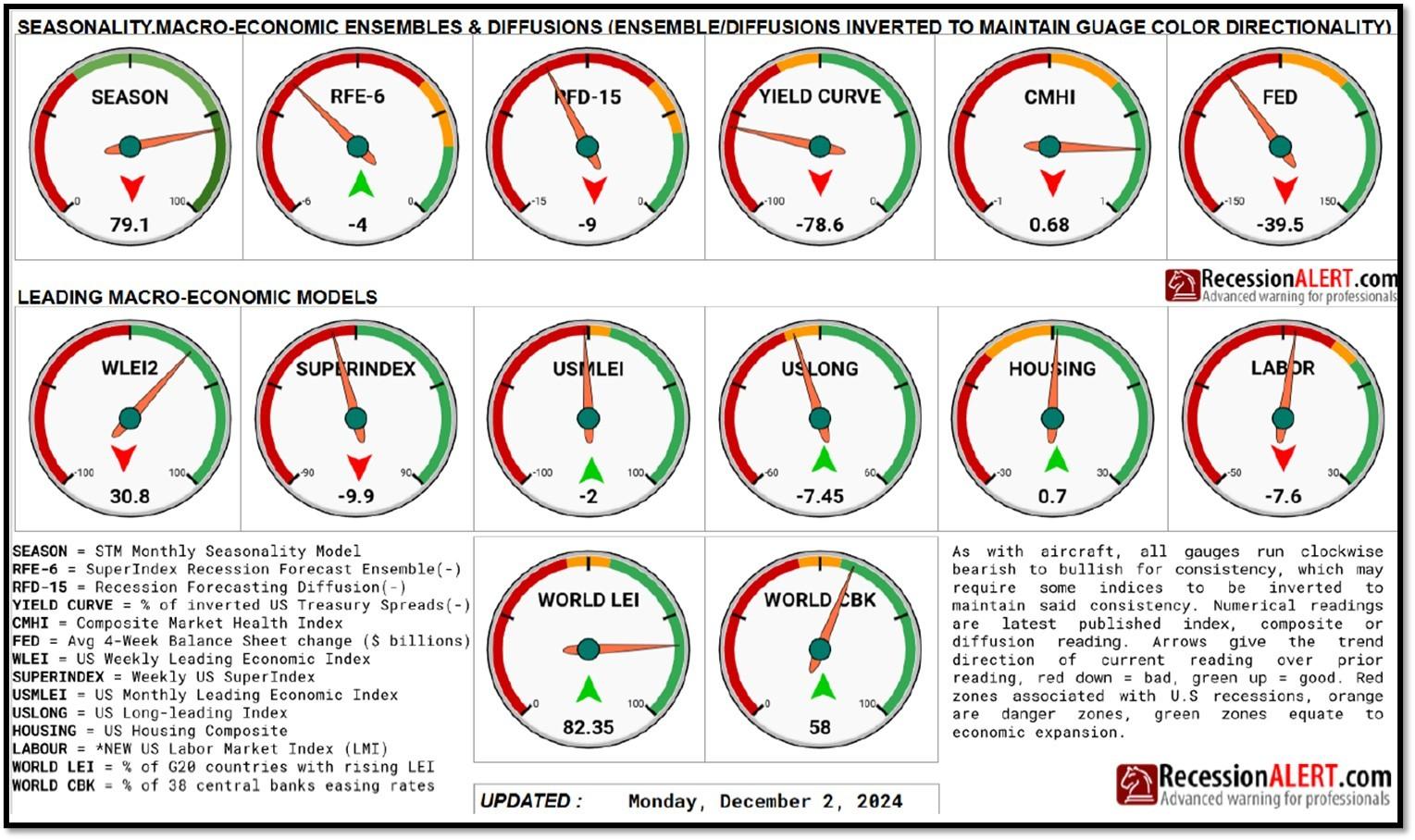

5F. Probability of U.S. falling into Recession within 3 to 4 months is currently at 68.53% (with data as of 12/2/2024 – Next Report 12/16/2024) according to RecessionAlert Research. Last release’s data was at 65.65%. This report is updated every two weeks. REF: RecessionAlertResearch

5G. Yield Curve as of 12/9/2024 is showing Flattening. Spread on the 10-yr Treasury Yield (4.19%) minus yield on the 2-yr Treasury Yield (4.12%) is currently at 7 bps. REF: Stockcharts The yield curve—specifically, the spread between the interest rates on the ten-year Treasury note and the three-month Treasury bill—is a valuable forecasting tool. It is simple to use and significantly outperforms other financial and macroeconomic indicators in predicting recessions two to six quarters ahead. REF: NYFED

5H. Recent Yields in 10-Year Government Bonds. REF: Source is from Bloomberg.com, dated 12/9/2024, rates shown below are as of 12/9/2024, subject to change.

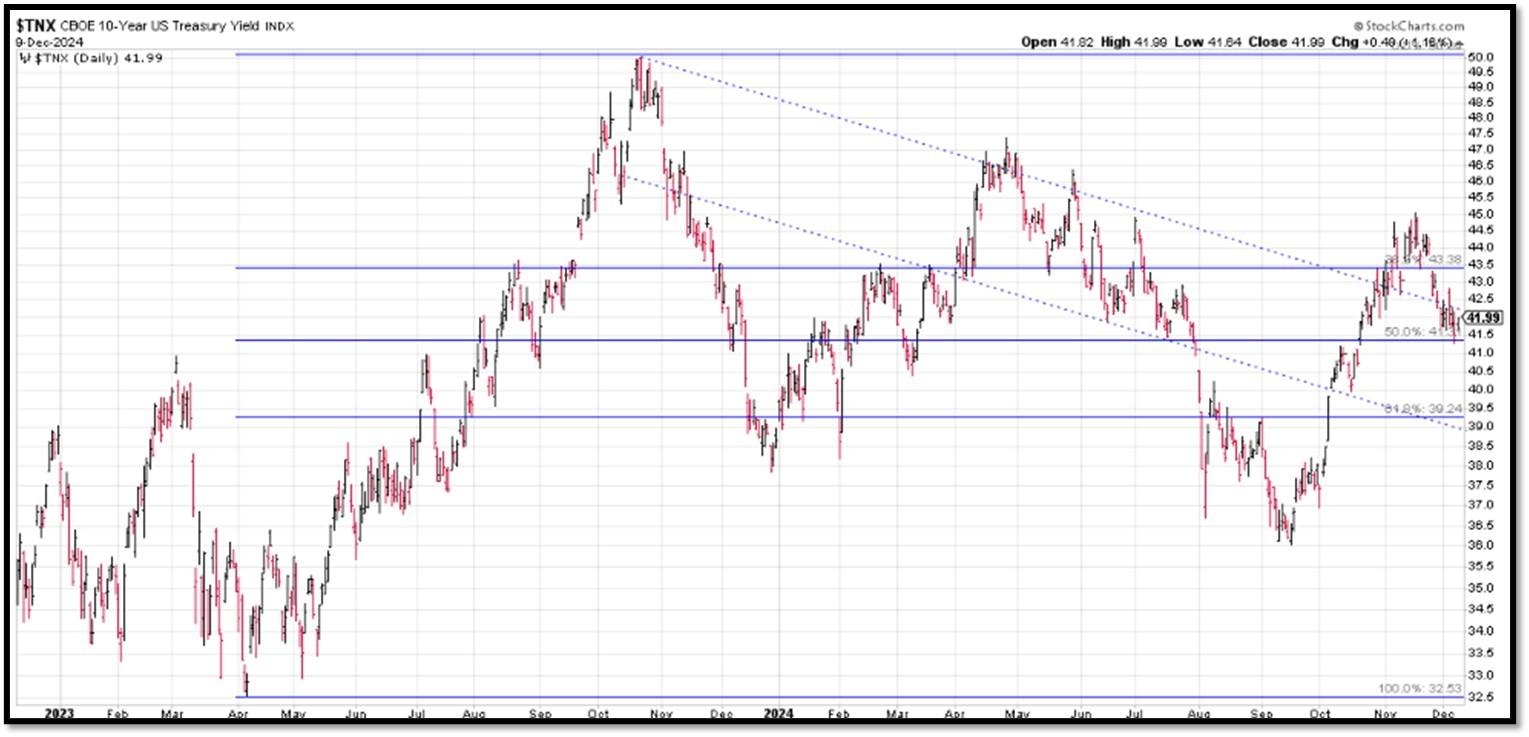

The 10-Year US Treasury Yield… REF: StockCharts1, StockCharts2

The 10-year yield – Spiked towards top of trend…

10-Year Real Interest Rate at 1.96321% as of 11/13/24. REF: REAINTRATREARAT10Y

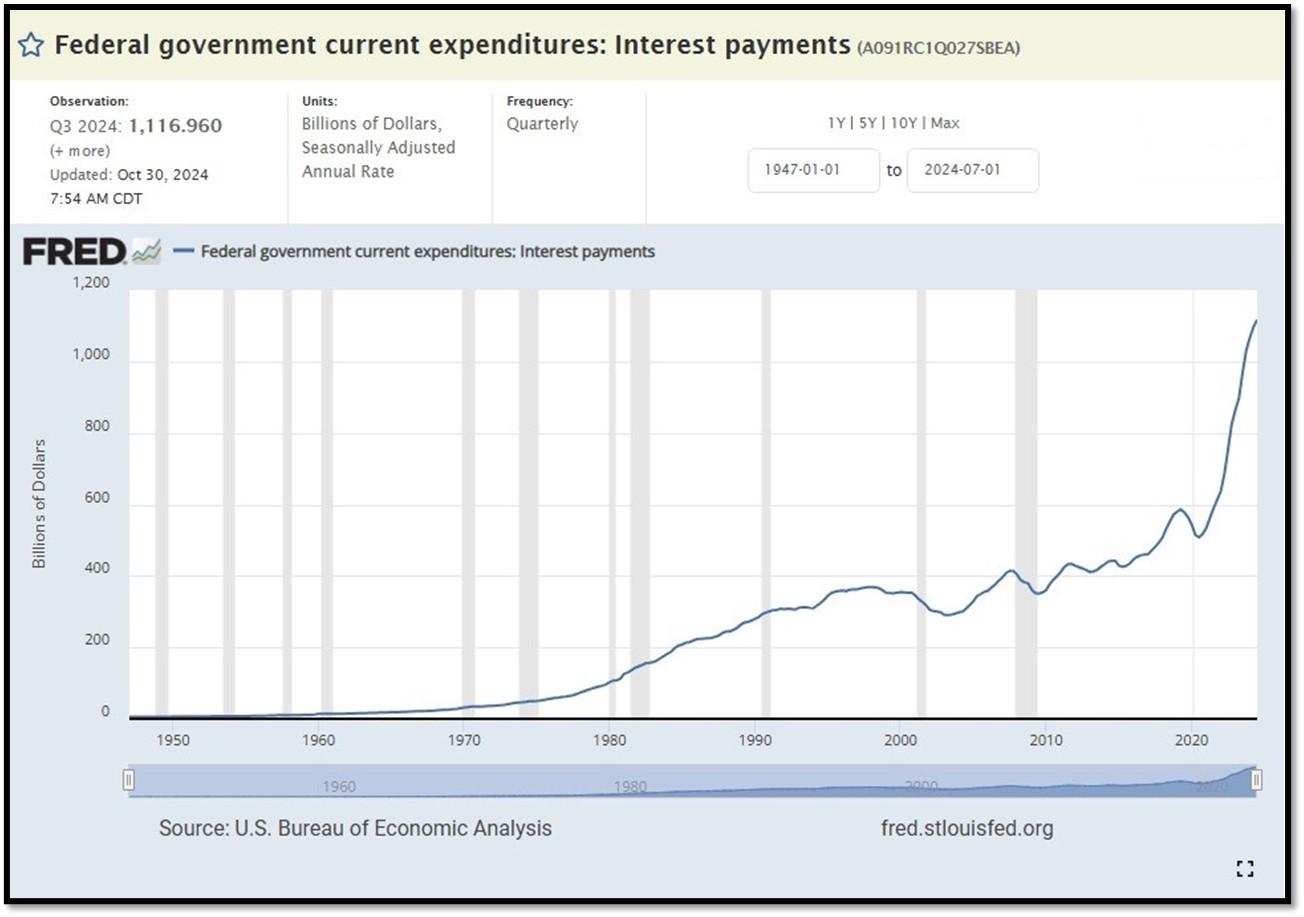

Federal government Interest Payments increased $20B+ to $1.1166 Trillion as of Q3-2024. REF: FRED-A091RC1Q027SBEA

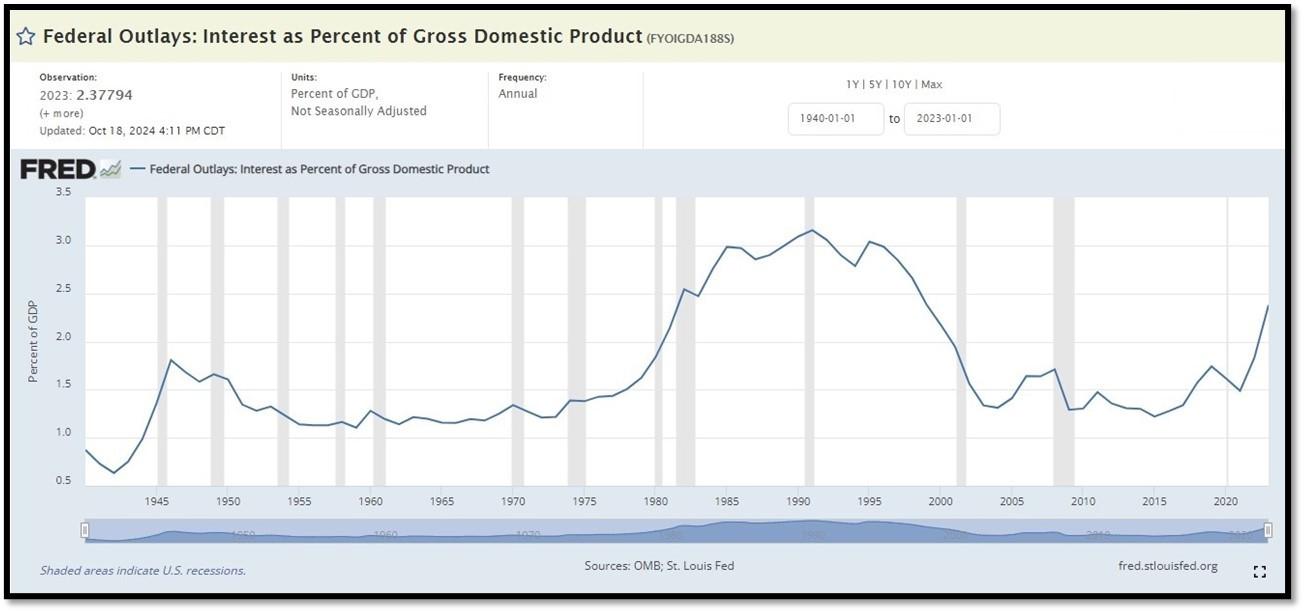

Interest payments as a percentage of GDP increased from 1.84853 in 2022 to 2.37794 as of 10/18/24. REF: FRED-FYOIGDA188S

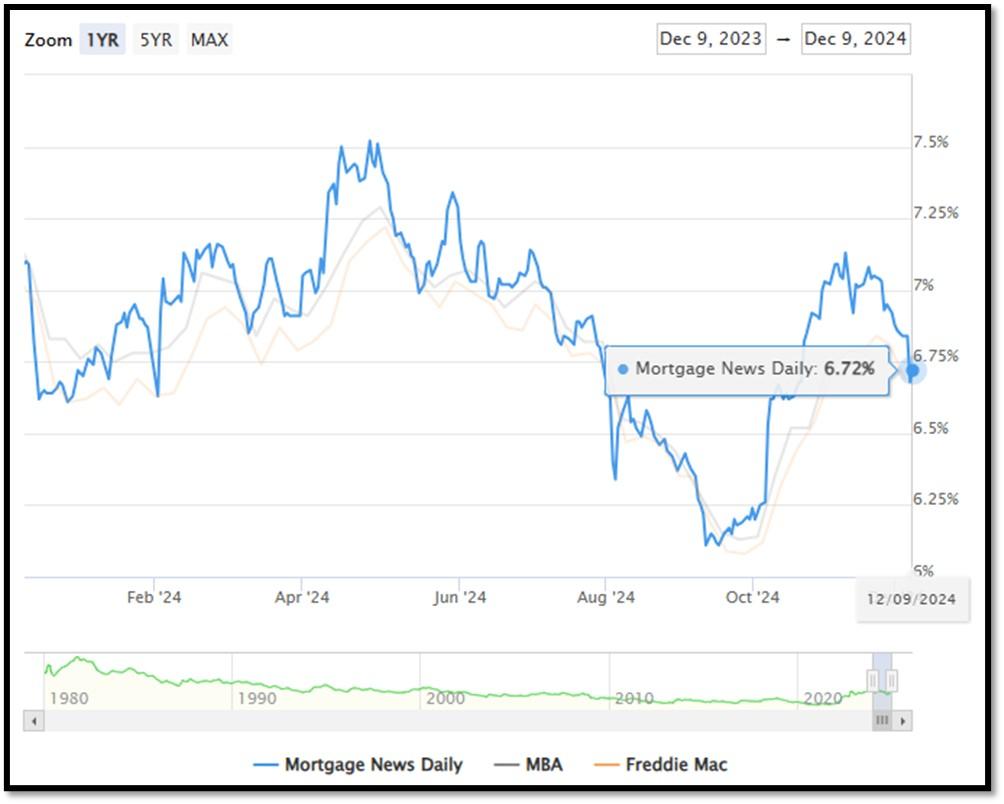

5I. (12/9/2024) Today’s National Average 30-Year Fixed Mortgage Rate is 6.72% (All Time High was 8.03% on 10/19/23). Last week’s data was 6.91%. This rate is the average 30-year fixed mortgage rates from several different surveys including Mortgage News Daily (daily index), Freddie Mac (weekly survey), Mortgage Bankers Association (weekly survey) and FHFA (monthly survey). REF: MortgageNewsDaily, Today’s Average Rate

The recent spike in the 30-year fixed-rate jumbo mortgage to 6.91%, compared to Freddie Mac’s rate at 6.81% and the Mortgage Bankers Association (MBA) rate at 6.73%, highlights key differences in the mortgage market. Jumbo mortgages, which exceed the conforming loan limits set by government agencies like Freddie Mac, typically carry higher interest rates because they are riskier for lenders. These loans are not backed by government entities, which increases the risk for lenders and, consequently, leads to higher rates. In contrast, Freddie Mac and MBA provide averages for conforming loans, which meet federal guidelines and have lower risk due to government backing, keeping their rates lower.

(11/11/24) Housing Affordability Index for Aug = 98.6 // July = 95 // June = 93.3 // May = 93.1 // April = 95.9 // March = 101.1 // February = 103.0. Data provided by Yardeni Research. REF: Yardeni

5J. Velocity of M2 Money Stock (M2V) with current read at 1.389 as of (Q2-2024 updated 10/30/2024). Previous quarter’s data was 1.385. The velocity of money is the frequency at which one unit of currency is used to purchase domestically- produced goods and services within a given time period. In other words, it is the number of times one dollar is spent to buy goods and services per unit of time. If the velocity of money is increasing, then more transactions are occurring between individuals in an economy. Current Money Stock (M2) report can be viewed in the reference link. REF: St.LouisFed-M2V

M2 consists of M1 plus (1) small-denomination time deposits (time deposits in amounts of less than $100,000) less IRA and Keogh balances at depository institutions; and (2) balances in retail MMFs less IRA and Keogh balances at MMFs. Seasonally adjusted M2 is constructed by summing savings deposits (before May 2020), small-denomination time deposits, and retail MMFs, each seasonally adjusted separately, and adding this result to seasonally adjusted M1. Board of Governors of the Federal Reserve System (US), M2 [M2SL], retrieved from FRED, Federal Reserve Bank of St. Louis; Updated on November 26, 2024. REF: St.LouisFed-M2

Money Supply M0 in the United States decreased to 5,567,200 USD Million in October from 5,588,400 USD Million in September of 2024. Money Supply M0 in the United States averaged 1,155,032.53 USD Million from 1959 until 2024, reaching an all-time high of 6,413,100 USD Million in December of 2021 and a record low of 48,400 USD Million in February of 1961. REF: TradingEconomics, M0

5K. In November, the Consumer Price Index for All Urban Consumers rose 0.3 percent, seasonally adjusted, and rose 2.7 percent over the last 12 months, not seasonally adjusted. The index for all items less food and energy increased 0.3 percent in November (SA); up 3.3 percent over the year (NSA). December 2024 CPI data are scheduled to be released on January 15, 2024, at 8:30AM-ET. REF: BLS, BLS.GOV

5L. Technical Analysis of the S&P500 Index. Click onto reference links below for images.

- Short-term Chart: Bullish on 12/9/2024 – REF: Short-term S&P500 Chart by Marc Slavin (Click Here to Access Chart)

- Medium-term Chart: Bullish on 12/9/2024 – REF: Medium-term S&P500 Chart by Marc Slavin (Click Here to Access Chart)

- Market Timing Indicators – S&P500 Index as of 12/9/2024 – REF: S&P500 Charts (7 of them) by Joanne Klein’s Top 7 (Click Here to Access Updated Charts)

- A well-defined uptrend channel shown in green with S&P500 still on up trend. REF: Stockcharts

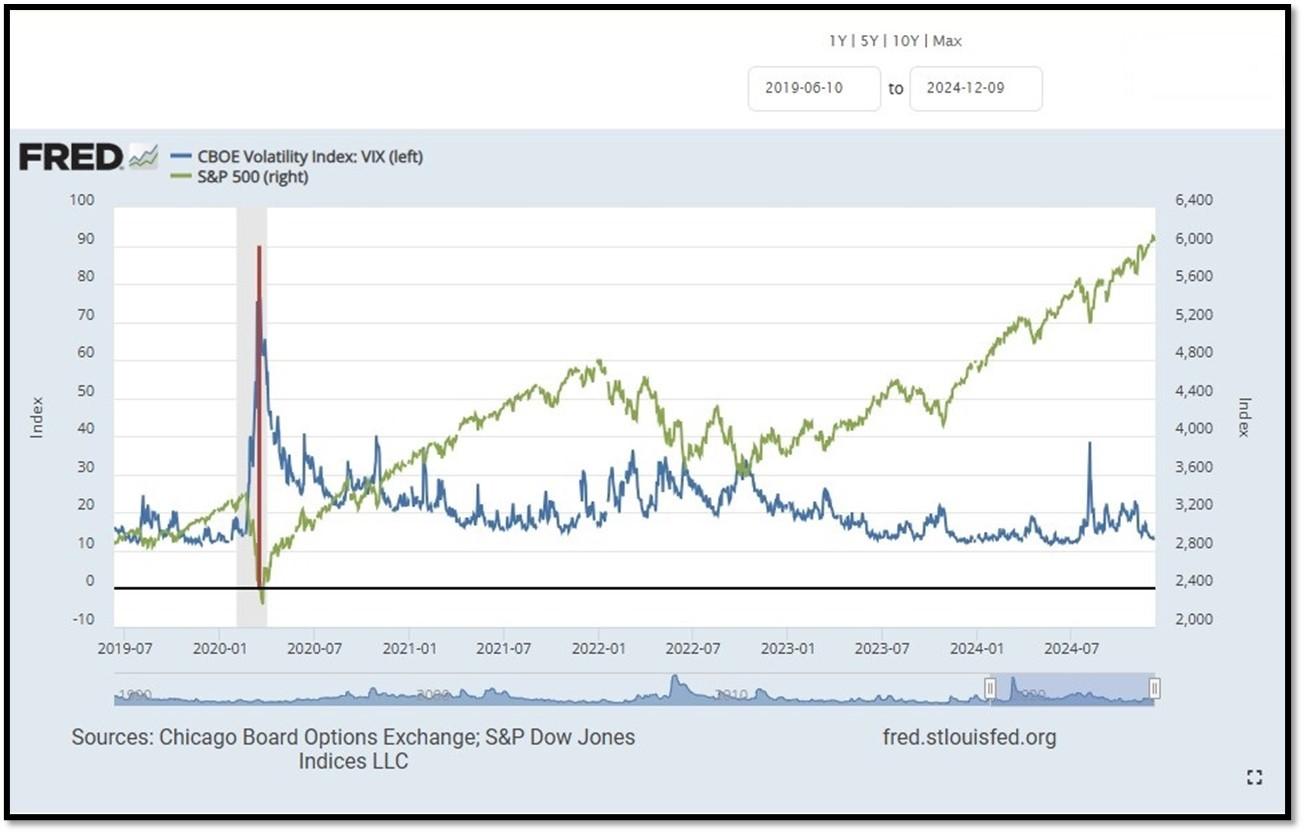

- S&P500 and CBOE Volatility Index (VIX) as of 12/9/2024. REF: FRED, Today’s Print

5M. Most recent read on the Crypto Fear & Greed Index with data as of 12/10/2024au is 78 (Extreme Greed). Last week’s data was 76 (Extreme Greed) (1-100). Fear & Greed Index – A Contrarian Data. The crypto market behavior is very emotional. People tend to get greedy when the market is rising which results in FOMO (Fear of missing out). Also, people often sell their coins in irrational reaction of seeing red numbers. With the Crypto Fear and Greed Index, the data try to help save investors from their own emotional overreactions. There are two simple assumptions:

- Extreme fear can be a sign that investors are too worried. That could be a buying opportunity.

- When Investors are getting too greedy, that means the market is due for a correction.

Therefore, the program for this index analyzes the current sentiment of the Bitcoin market and crunch the numbers into a simple meter from 0 to 100. Zero means “Extreme Fear”, while 100 means “Extreme Greed”. REF: Alternative.me, Today’sReading

Bitcoin – 10-Year & 2-Year Charts. REF: Stockcharts10Y, Stockcharts2Y

Len writes much of his own content, and also shares helpful content from other trusted providers like Turner Financial Group (TFG).

The material contained herein is intended as a general market commentary, solely for informational purposes and is not intended to make an offer or solicitation for the sale or purchase of any securities. Such views are subject to change at any time without notice due to changes in market or economic conditions and may not necessarily come to pass. This information is not intended as a specific offer of investment services by Dedicated Financial and Turner Financial Group, Inc.

Dedicated Financial and Turner Financial Group, Inc., do not provide tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.

Any hyperlinks in this document that connect to Web Sites maintained by third parties are provided for convenience only. Turner Financial Group, Inc. has not verified the accuracy of any information contained within the links and the provision of such links does not constitute a recommendation or endorsement of the company or the content by Dedicated Financial or Turner Financial Group, Inc. The prices/quotes/statistics referenced herein have been obtained from sources verified to be reliable for their accuracy or completeness and may be subject to change.

Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. The views and strategies described herein may not be suitable for all investors. To the extent referenced herein, real estate, hedge funds, and other private investments can present significant risks, including loss of the original amount invested. All indexes are unmanaged, and an individual cannot invest directly in an index. Index returns do not include fees or expenses.

Turner Financial Group, Inc. is an Investment Adviser registered with the United States Securities and Exchange Commission however, such registration does not imply a certain level of skill or training and no inference to the contrary should be made. Additional information about Turner Financial Group, Inc. is also available at www.adviserinfo.sec.gov. Advisory services are only offered to clients or prospective clients where Turner Financial Group, Inc. and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Turner Financial Group, Inc. unless a client service agreement is in place.