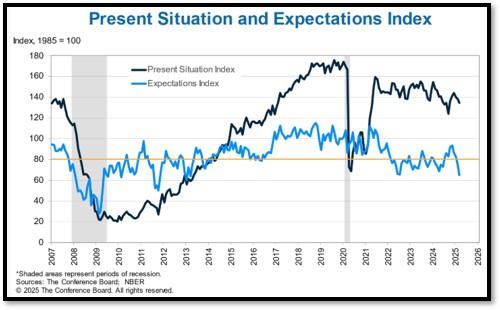

- 1. Recent economic news sent ripples through the stock market as consumer confidence plummeted to a 12-year low, heightening recession fears. No, I don’t believe recession is upon us in the near term. However,…

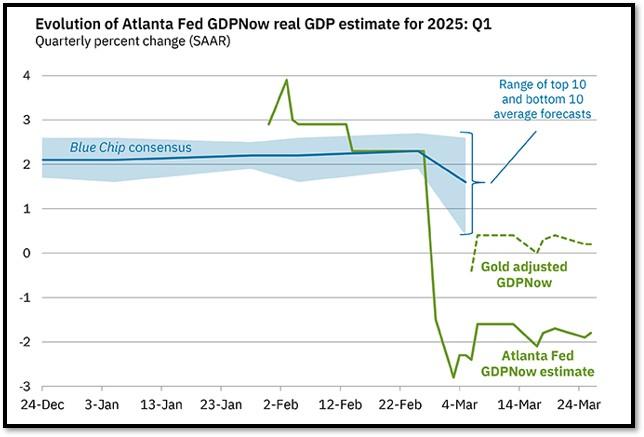

- 2. The Atlanta Fed’s GDPNow model showing a -1.8% real GDP growth estimate for Q1 2025 (as of March 26) versus the alternative model’s 0.2% forecast highlights an interesting tweak: adjusting for imports and exports of gold. So why exclude gold?

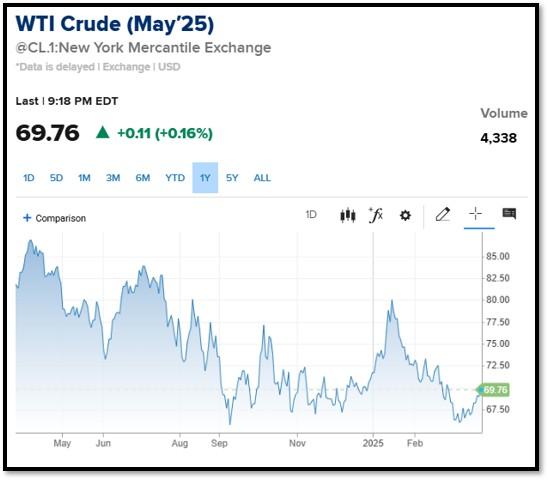

- 3. In early 2025, energy stocks have emerged as standout performers in the stock market, with the sector rising 8.9% while the S&P 500 has declined by 1.8%.

- 4. World Watch

- 5. Quant & Technical Corner

1. Recent economic news sent ripples through the stock market as consumer confidence plummeted to a 12-year low, heightening recession fears. No, I don’t believe recession is upon us in the near term. However,…

the Conference Board reported its Consumer Confidence Index dropped to 92.9 in March, a significant decline that marked the fourth consecutive month of waning optimism among Americans. A key measure within the report, the Expectations Index, fell sharply to 65.2—well below the critical threshold of 80 that often signals an impending recession—reflecting deep consumer pessimism about future income, business conditions, and job prospects. This downturn, coupled with concerns over persistent inflation, potential tariffs, and policy uncertainty, has amplified economic anxiety, contributing to a volatile stock market response as investors grapple with the prospect of slowing growth. The stark drop in confidence, alongside reports of tepid retail sales and cautious corporate outlooks from major retailers, underscores a fragile economic landscape that could further unsettle Wall Street in the weeks ahead. REF: ConferenceBoard, Website

2. The Atlanta Fed’s GDPNow model showing a -1.8% real GDP growth estimate for Q1 2025 (as of March 26) versus the alternative model’s 0.2% forecast highlights an interesting tweak: adjusting for imports and exports of gold. So why exclude gold?

- Volatility and Noise: Gold trade is notoriously erratic—big swings in imports or exports can distort GDP without reflecting core economic health. For instance, if a firm stockpiles $1 billion in gold imports (like in Q3 2024, when imports spiked 20% per Census data), it boosts nominal GDP via higher imports (a negative in the GDP formula: GDP = C + I + G + (X – M)). But this doesn’t mean consumers are spending more or factories are humming—it’s just bullion moving around. Excluding it smooths out these blips, giving a clearer picture of production and consumption.

- Non-Productive Nature: Gold often acts as a store of value or hedge, not a productive input like steel or silicon. When exports surge—say, $500 million in Q1 2025—it lifts net exports (X – M), inflating GDP. Yet, this might reflect investor panic (e.g., fleeing to gold amid tariff fears) rather than industrial strength. The alternative model aims to focus on goods and services tied to real economic output, not speculative flows.

- Historical Precedent: Gold’s impact has skewed GDP before. In 2013, a gold export surge added 0.3% to Q2 growth, per BEA revisions, but later data showed it overstated activity—prompting calls for adjustments. The Atlanta Fed’s alternative model, detailed in a 2022 methodology update, builds on this, isolating gold to better match final BEA estimates, which often revise out such anomalies.

- Trade Anomalies: Q1 2025’s -1.8% GDPNow versus 0.2% adjusted forecast suggests gold trade skewed the unadjusted number. Census data hints at a possible gold import drop or export jump—perhaps tied to Trump’s tariff threats (25% on Canada/Mexico) or safe-haven buying amid market selloffs (S&P 500 down 2.7% March 10). Without gold, the 0.2% hints at a less dire economy, aligning with your rolling recession recovery view.

An unusual increase in import data ahead of April 2 (covering January, February, and March) is also skewing the numbers. REF: GDPnow, Today’s GDPnow, Adjusted GDPnow

3. In early 2025, energy stocks have emerged as standout performers in the stock market, with the sector rising 8.9% while the S&P 500 has declined by 1.8%.

This surge is notable given a concurrent 4% drop in oil prices, suggesting that factors beyond commodity prices are influencing investor behavior. Many investors are gravitating toward energy stocks, attracted by their relatively low valuations, substantial dividend yields, and a cautiously optimistic outlook for future oil demand. Companies like Exxon Mobil and Chevron have experienced price increases despite declining earnings estimates, indicating a valuation-driven rally rather than one based on improving fundamentals.

However, this upward momentum in energy stocks may be short-lived. The gains appear fragile as they are primarily driven by increased valuations without corresponding improvements in earnings prospects. Rising risks, including potential recessions and policy impacts, suggest that the current rally may not be sustainable. Additionally, the increased confidence in long-term oil demand, possibly attributed to political support for the oil industry, might wane if market conditions change. Investors should exercise caution, recognizing that the current enthusiasm for energy stocks may not persist in the face of evolving economic and policy landscapes. Click onto picture below to access video from Tom Lee of Fundstrat. REF: BARRON’S

With the current macro-economic backdrop, below are areas we currently favor:

- Fixed Income – Short-term Corporates (Low-Beta)

- Fixed Income – Corporates High Yield as Opportunistic Allocation (Low-Beta)

- Businesses that contribute to and benefit from AI & Automation (Market-Risk)

- Communications (Market-Risk)

- Cyber-Security (Market-Risk)

- Financials (Market-Risk)

- Small Cap & Mid Cap Stocks (Market-Risk)

- Biotechnology (Market-Risk)

- Gold & Digital Asset – Bitcoin (Market-Risk/Hedge)

4. World Watch

4A. A Tale of Two Commodities – Oil & Gas. Over the past year, oil and natural gas prices have diverged significantly, moving in opposite directions due to distinct supply and demand dynamics.

U.S. natural gas prices have remained relatively subdued, primarily influenced by mild weather conditions that reduced heating demand. However, structural demand remains supported by the rising energy needs of data centers and AI-driven computing, which rely heavily on consistent electricity generation. Despite the moderation in spot prices, the long-term outlook for natural gas remains firm due to its growing role in powering the digital economy, especially as renewables remain intermittent and nuclear remains politically constrained in some regions.

In contrast, oil prices have faced downward pressure as global supply has steadily increased. The U.S. and other producers have raised output, while transportation demand—historically a key driver of crude consumption—has seen only modest gains. Factors such as more fuel-efficient vehicles, slower travel growth, and lingering concerns over global economic growth have limited the upside for oil. With inventories stabilizing and no major supply shocks on the horizon, oil markets have priced in this balance, keeping prices contained. Together, these trends reflect a decoupling between the two commodities, each responding to a distinct set of economic and technological forces. REF: CNBC, WSJ, OPEC

4B. It’s Spring-Cleaning Time in China… In response to mounting challenges in the real estate sector, Chinese banks are intensifying efforts to dispose of non-performing property loans to bolster economic stability.

In 2024, the financial industry disposed of a record 3.8 trillion yuan (approximately $532 billion) in bad assets, as reported by the banking regulator. Regulators have urged major institutions, including the Industrial & Commercial Bank of China Ltd., to prioritize the write-off of soured property loans. Some banks have reportedly doubled their annual quotas for such disposals at local branches this year.

This proactive approach aims to clean up balance sheets and restore confidence in the financial system amid a prolonged property sector downturn. Developers like Sunac have undergone unprecedented debt restructurings, highlighting the severity of the crisis. By accelerating the disposal of bad loans, banks seek to mitigate risks, free up capital for new lending, and support broader economic recovery efforts. Losses from Chinese properties are ‘digestible by China’s banking system,’ according to May Yan of UBS, in a statement made two years ago. Click onto picture below to access video. REF: Bloomberg

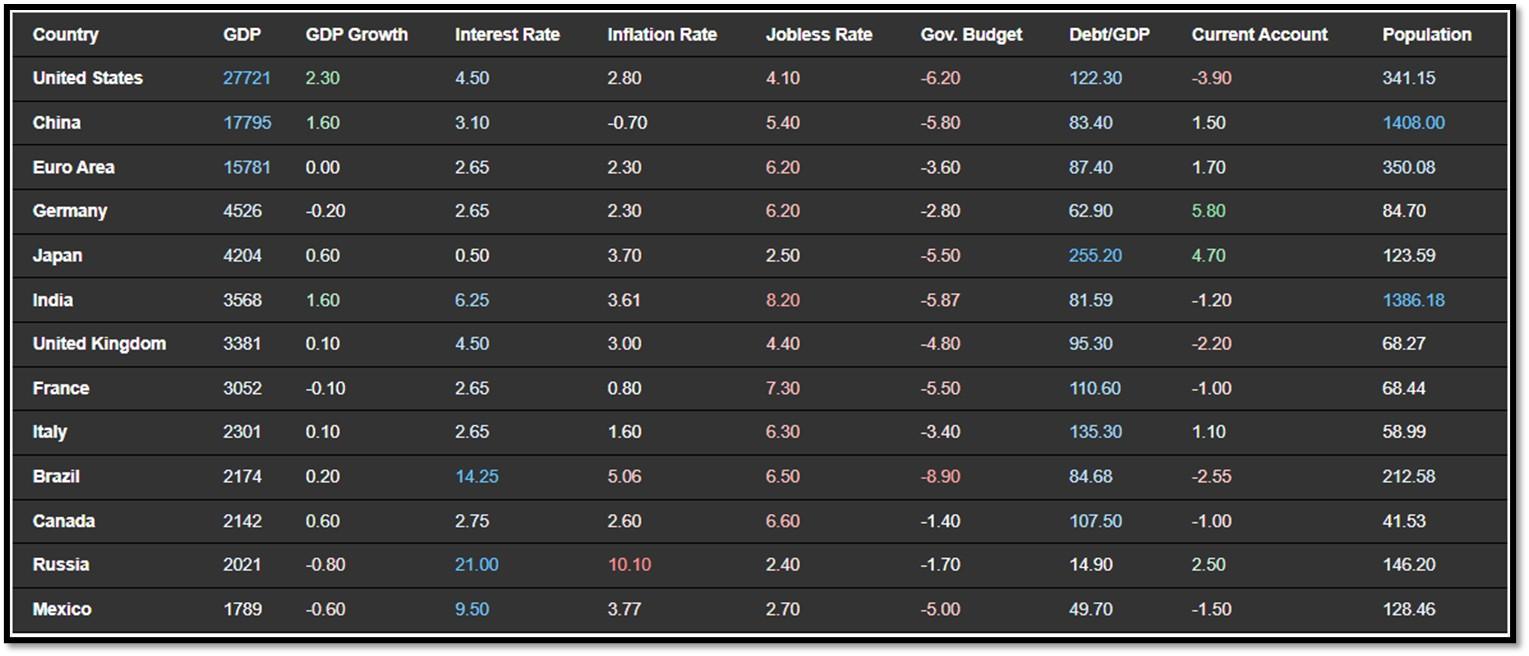

4C. Below is an updated snapshot of the current global state of economy according to TradingEconomics as of 3/24/2025.

REF: TradingEconomics

- Inflation Rate In the Euro Area decreased to 2.30 percent in February from 2.50 percent in January of 2025.

- The annual inflation rate in Japan fell to 3.7% in February 2025 from a 2-year high of 4.0% in the prior month, amid a sharp slowdown in prices of electricity (9.0% vs 18.0% in January )and gas (3.4% vs 6.8%) following the government’s reinstatement of energy subsidies.

- The Central Bank of Brazil raised its Selic rate by 100 bps to 14.25% in March 2025, aiming to bring inflation closer to the target.

- The annual inflation rate in Canada jumped to 2.6% in February of 2025 from 1.9% in the previous month, the highest in eight months, sharply above market expectations of 2.2% and ahead of the Bank of Canada’s forecast of 2.5%.

5. Quant & Technical Corner

Below is a selection of quantitative & technical data we monitor on a regular basis to help gauge the overall financial market conditions and the investment environment.

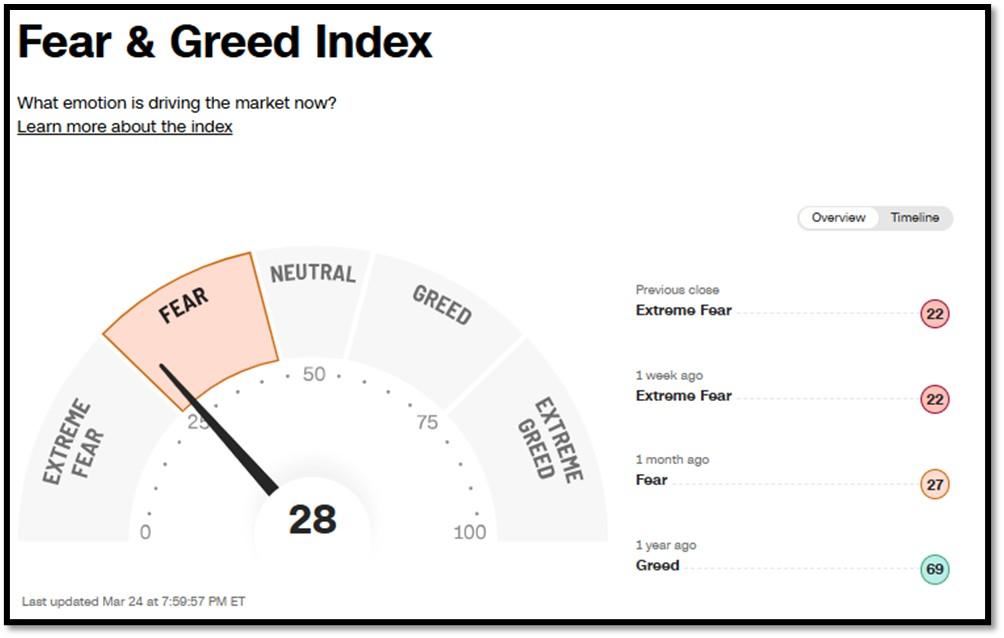

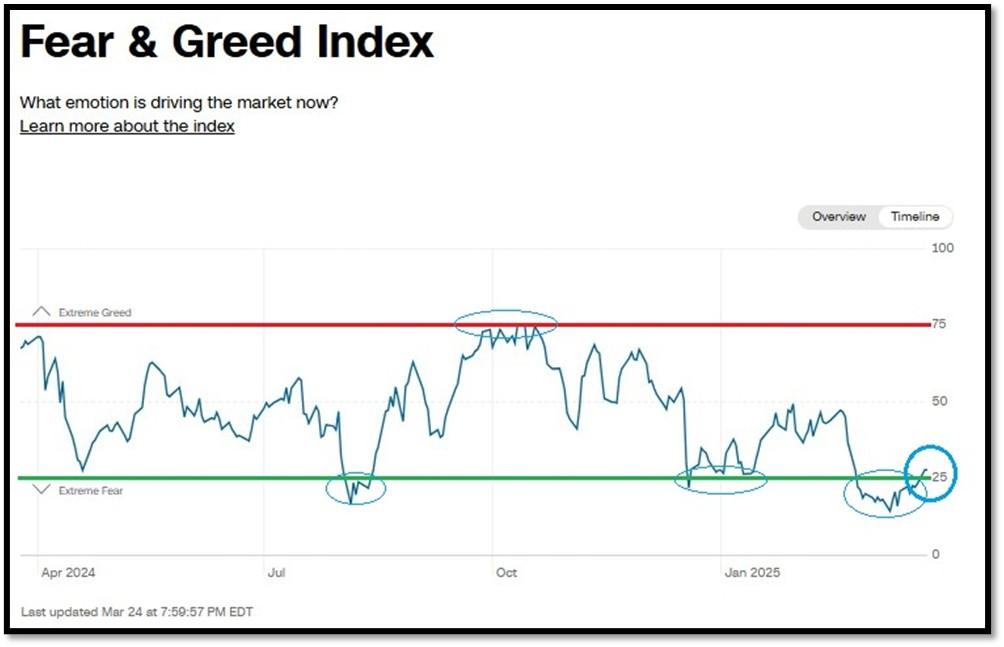

5A. Most recent read on the Fear & Greed Index with data as of 3/24/2025 – 7:59PM-ET is 28 (Fear). Last week’s data was 22 (Extreme Fear) (1-100). CNNMoney’s Fear & Greed index looks at 7 indicators (Stock Price Momentum, Stock Price Strength, Stock Price Breadth, Put and Call Options, Junk Bond Demand, Market Volatility, and Safe Haven Demand). Keep in mind this is a contrarian indicator! REF: Fear&Greed via CNNMoney

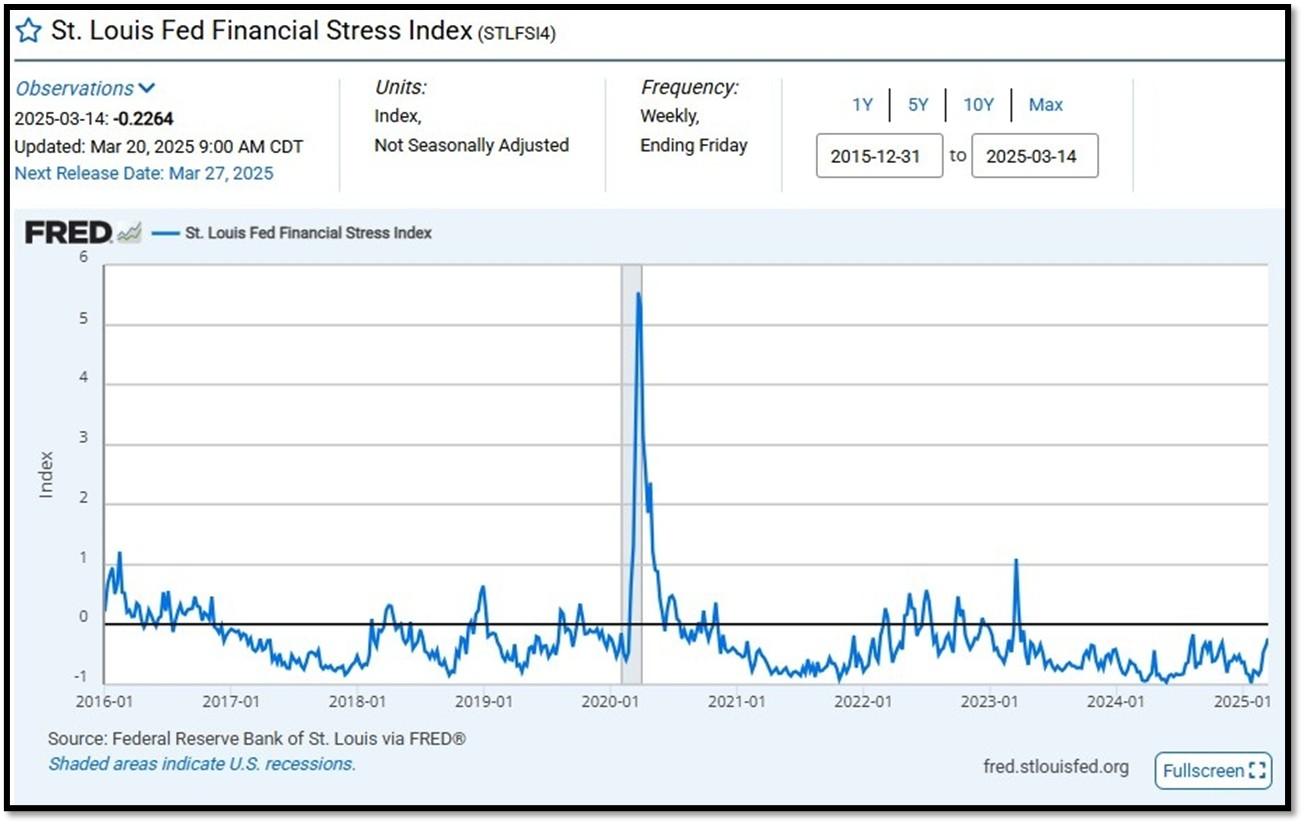

5B. St. Louis Fed Financial Stress Index’s (STLFSI4) most recent read is at –0.2264 as of March 20, 2025. Previous week’s data was -0.3601. A big spike up from previous readings reflecting the turmoil in the banking sector back in 2023. This weekly index is not seasonally adjusted. The STLFSI4 measures the degree of financial stress in the markets and is constructed from 18 weekly data series: seven interest rate series, six yield spreads and five other indicators. Each of these variables captures some aspect of financial stress. Accordingly, as the level of financial stress in the economy changes, the data series are likely to move together. REF: St. Louis Fed

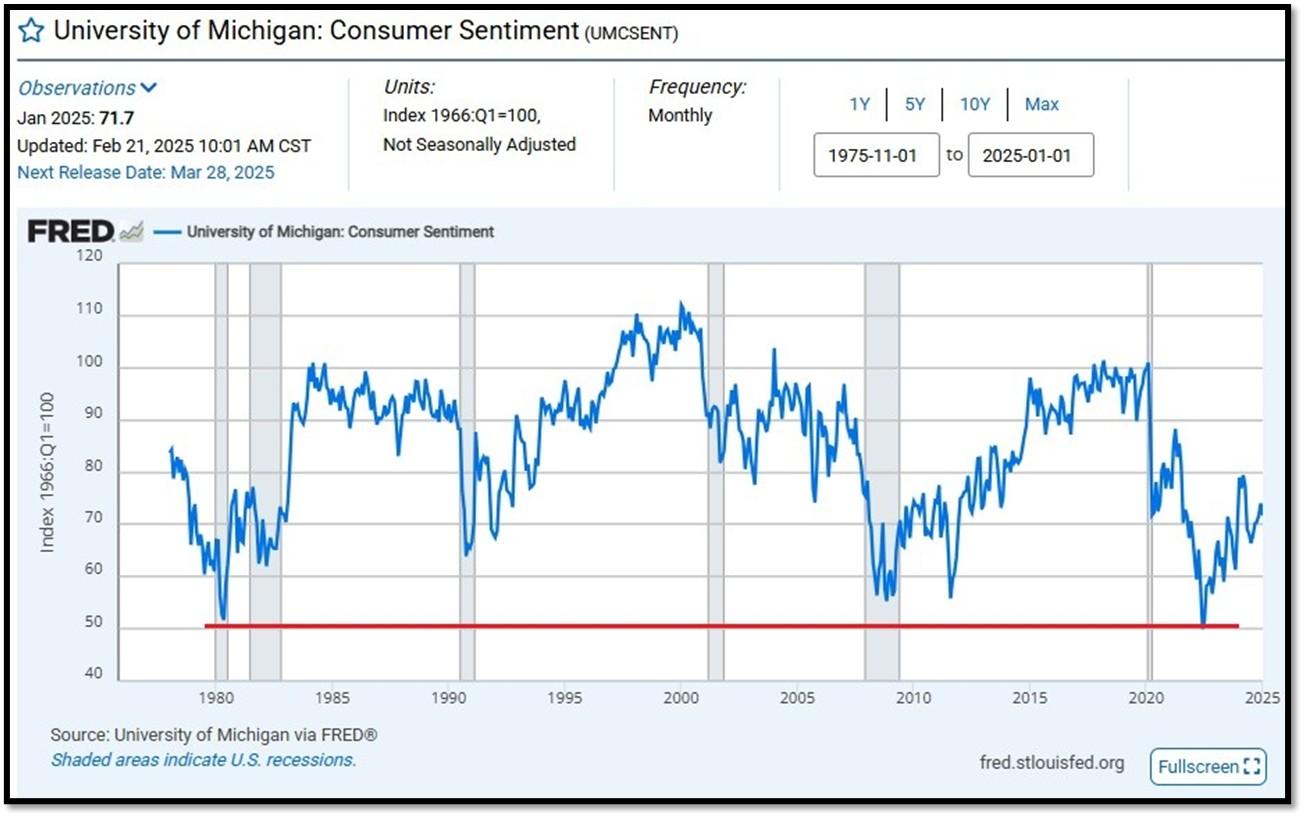

5C. University of Michigan, University of Michigan: Consumer Sentiment for January [UMCSENT] at 71.7, retrieved from FRED, Federal Reserve Bank of St. Louis, February 21, 2025. Back in June 2022, Consumer Sentiment hit a low point going back to April 1980. REF: UofM

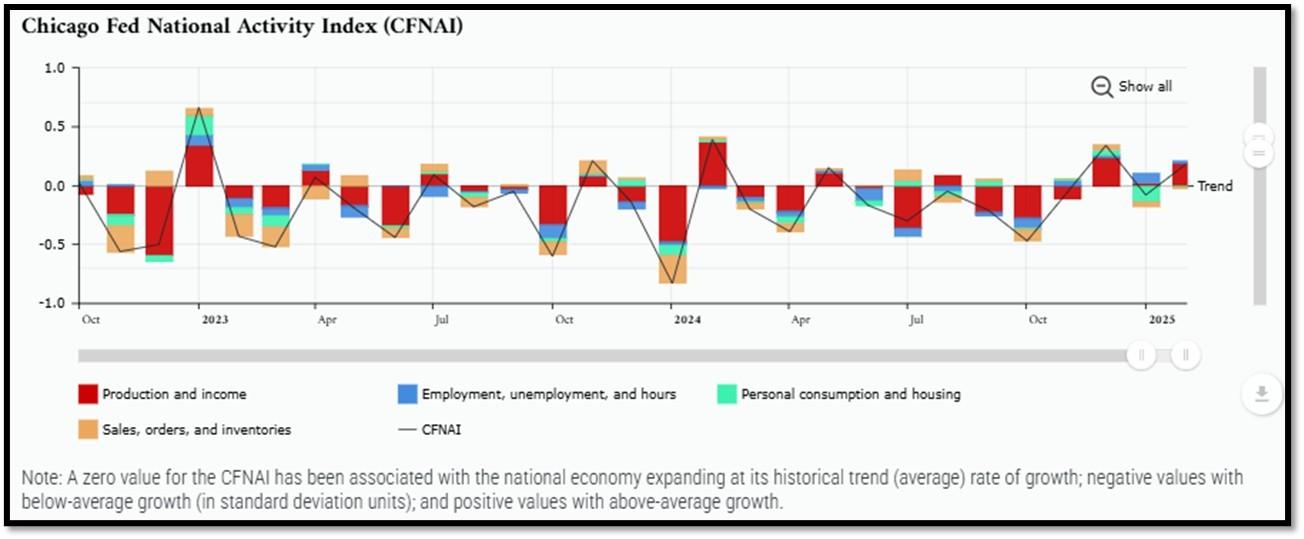

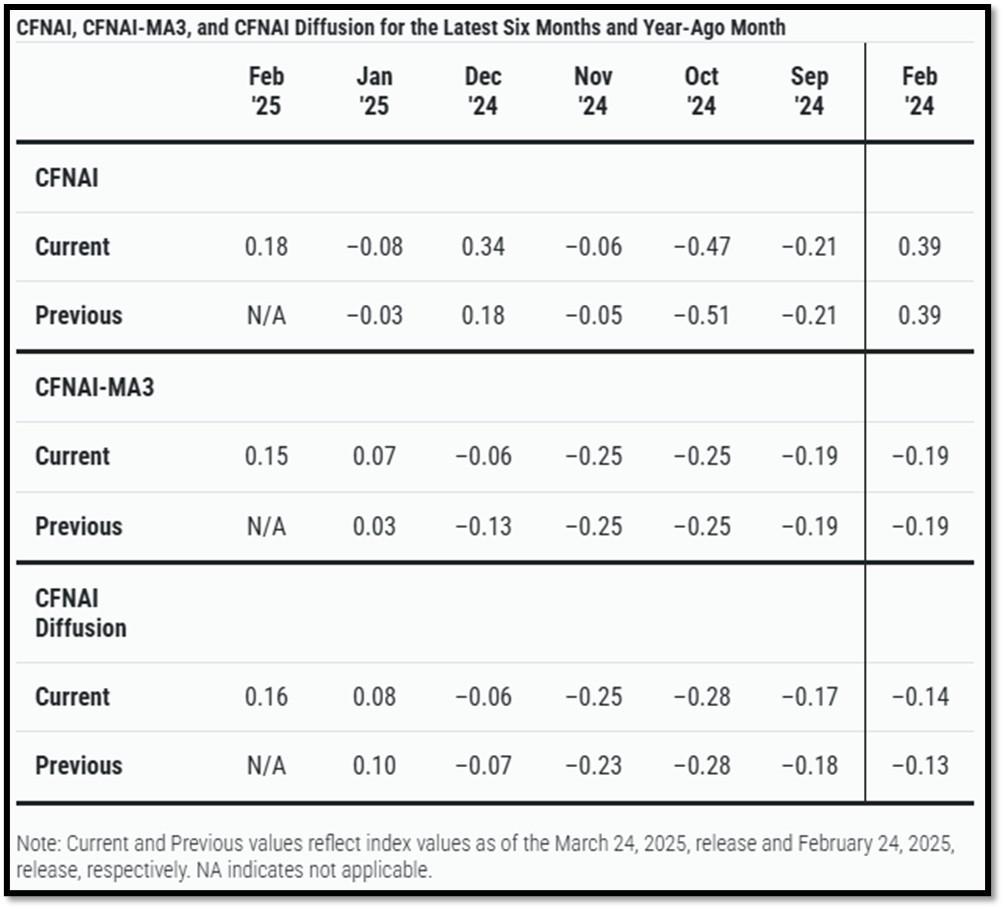

5D. The Chicago Fed National Activity Index (CFNAI) increased to +0.18 in February from –0.08 in January. Three of the four broad categories of indicators used to construct the index increased from January, and two categories made positive contributions in February. The index’s three-month moving average, CFNAI-MA3, increased to +0.15 in February from +0.07 in January. REF: ChicagoFed, February’s Report

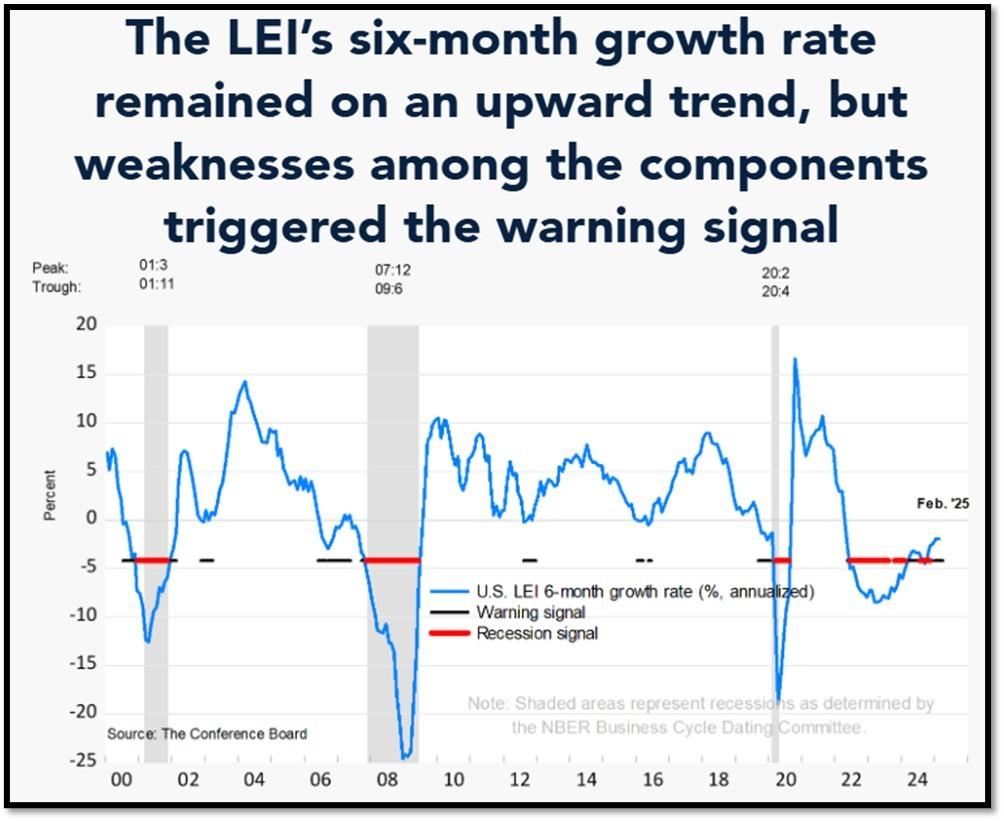

5E. (3/20/2025) The Conference Board Leading Economic Index (LEI) for the US declined by 0.3% in February 2025 to 101.1 (2016=100), after a 0.2% decline (revised from –0.3%) in January. Overall, the LEI fell by 1.0% in the six-month period ending February 2025, less than half of its rate of decline of –2.1% over the previous six months (February–August 2024). The composite economic indexes are the key elements in an analytic system designed to signal peaks and troughs in the business cycle. The indexes are constructed to summarize and reveal common turning points in the economy in a clearer and more convincing manner than any individual component. The CEI is highly correlated with real GDP. The LEI is a predictive variable that anticipates (or “leads”) turning points in the business cycle by around 7 months. Shaded areas denote recession periods or economic contractions. The dates above the shaded areas show the chronology of peaks and troughs in the business cycle. The ten components of The Conference Board Leading Economic Index® for the U.S. include: Average weekly hours in manufacturing; Average weekly initial claims for unemployment insurance; Manufacturers’ new orders for consumer goods and materials; ISM® Index of New Orders; Manufacturers’ new orders for nondefense capital goods excluding aircraft orders; Building permits for new private housing units; S&P 500® Index of Stock Prices; Leading Credit Index™; Interest rate spread (10-year Treasury bonds less federal funds rate); Average consumer expectations for business conditions. REF: ConferenceBoard, LEI Report for January (Released on 3/2/2025)

We have experienced a “rolling recession” since June 2022 and are only now emerging from it. However, authorities are not labeling it a recession due to high employment data.

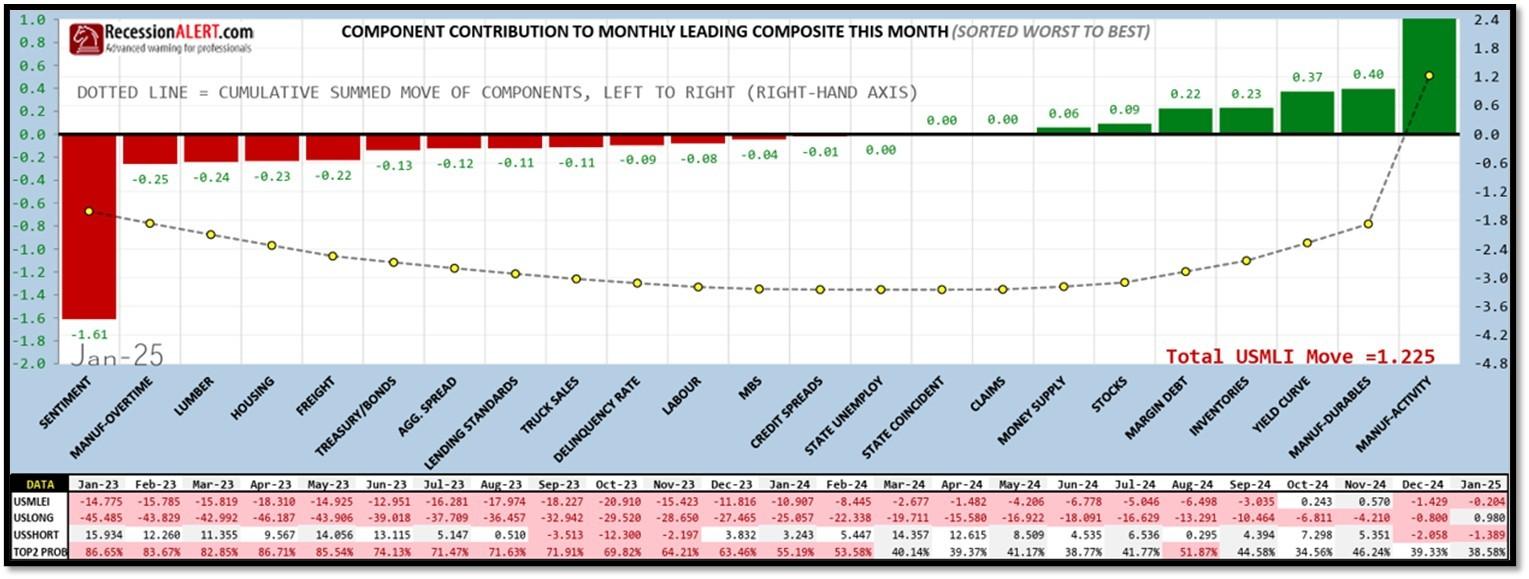

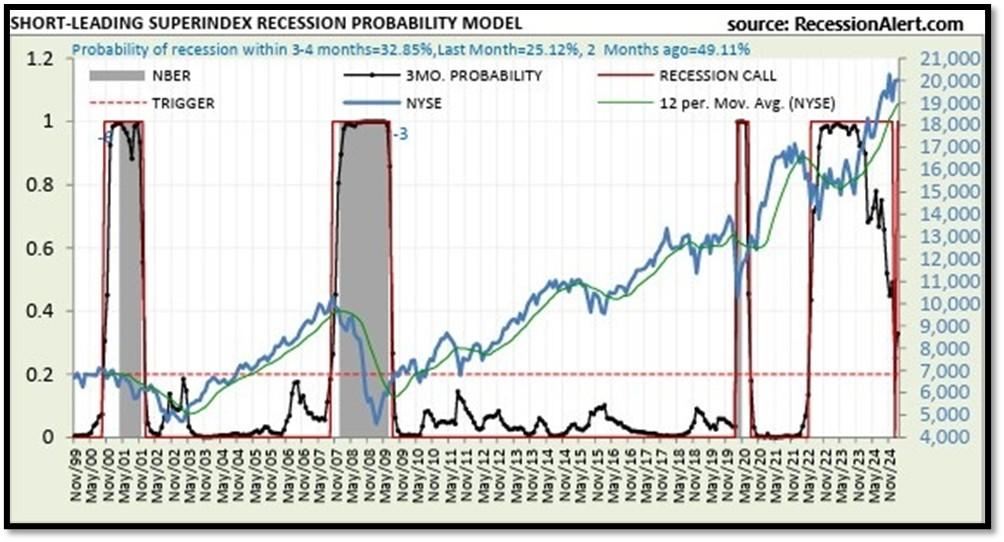

5F. Probability of U.S. falling into Recession within 3 to 4 months is currently at 32.85% (with data as of 03/10/2025 – Next Report 03/24/2025) according to RecessionAlert Research. Last release’s data was at 27.33%. This report is updated every two weeks. REF: RecessionAlertResearch

5G. Yield Curve as of 3/24/2025 is showing Normal. Spread on the 10-yr Treasury Yield (4.32%) minus yield on the 2-yr Treasury Yield (4.03%) is currently at 29bps. REF: Stockcharts The yield curve—specifically, the spread between the interest rates on the ten-year Treasury note and the three-month Treasury bill—is a valuable forecasting tool. It is simple to use and significantly outperforms other financial and macroeconomic indicators in predicting recessions two to six quarters ahead. REF: NYFED

![]()

5H. Recent Yields in 10-Year Government Bonds. REF: Source is from Bloomberg.com, dated 3/24/2025, rates shown below are as of 3/24/2025, subject to change.

![]()

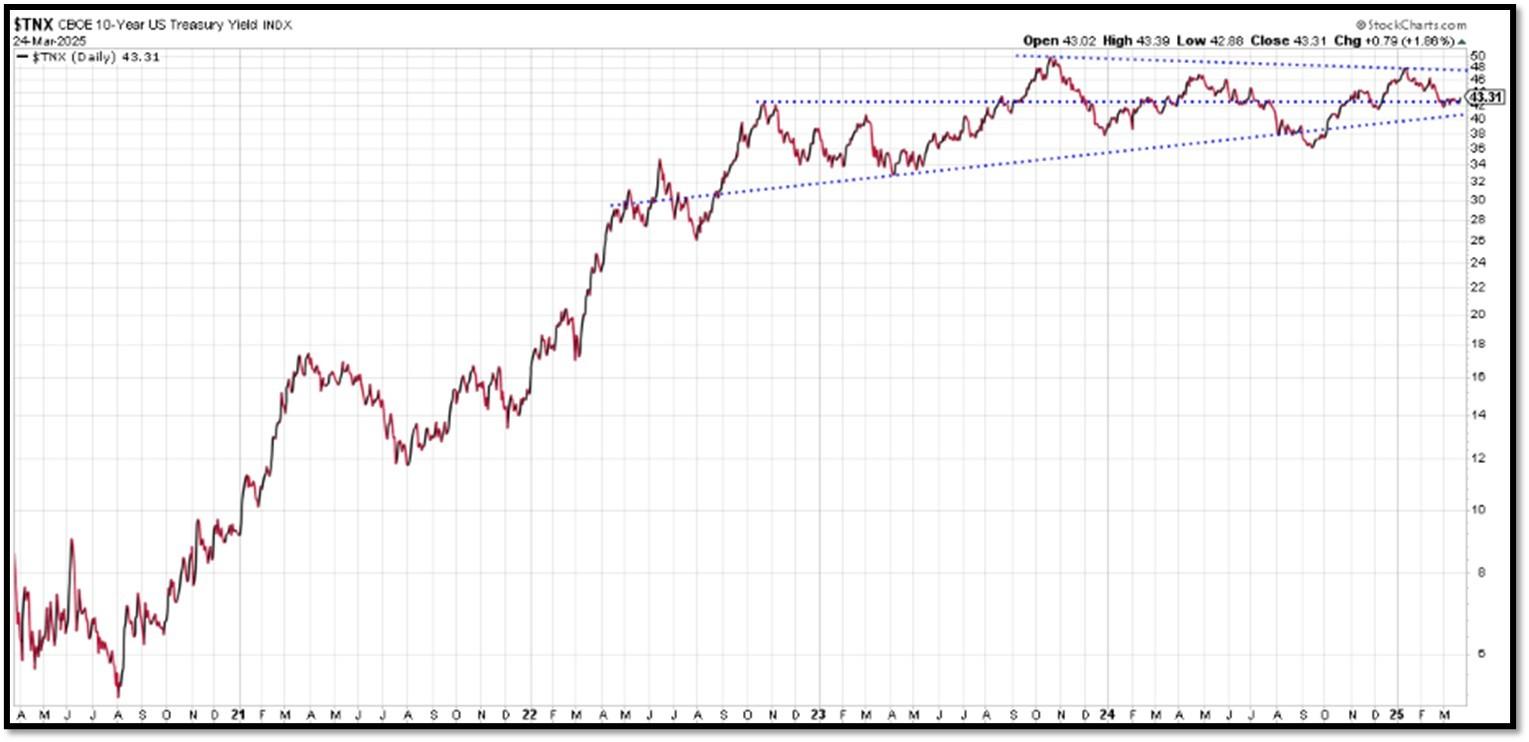

The 10-Year US Treasury Yield… The 10-Year Yield is indirectly related to inflation. I expect the 10-Year Yield to drop further as dis-inflation kicks in. REF: StockCharts1, StockCharts2

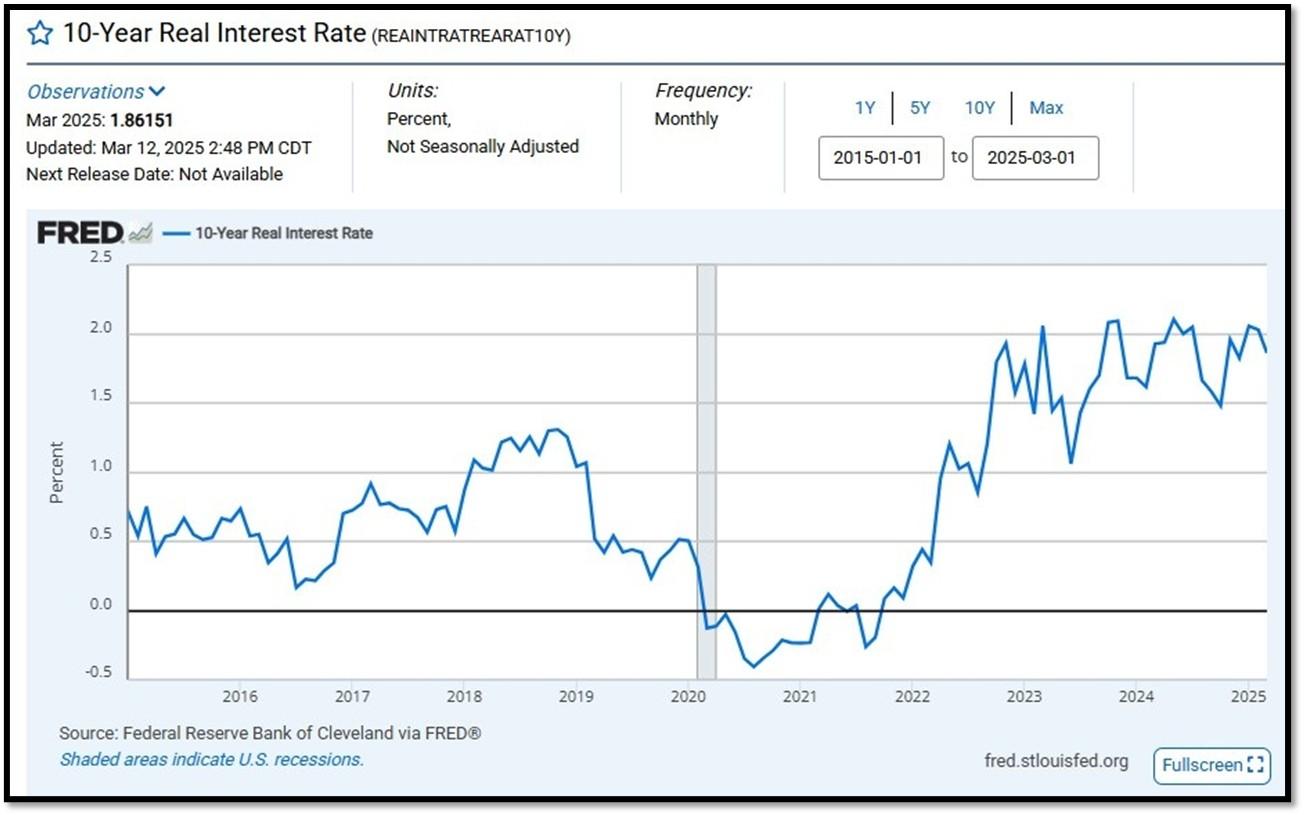

10-Year Real Interest Rate at 1.86151% as of 3/12/25. Last month’s data was 2.03128%. REF: REAINTRATREARAT10Y

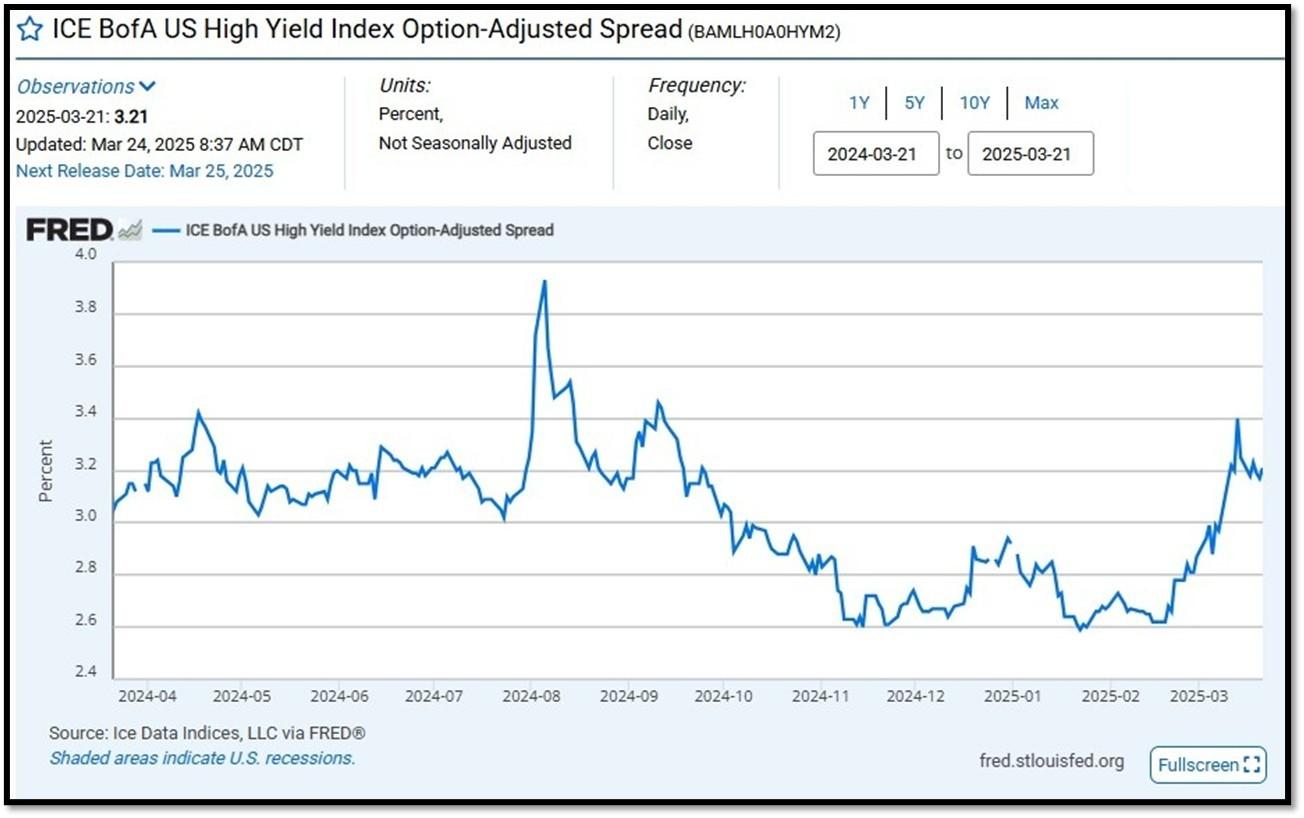

ICE BofA US High Yield Index Option-Adjusted Spread (BAMLH0A0HYM2) currently at 3.21 as of March 24, 2025. This is a key indicator of market sentiment, particularly regarding risk and economic health. At its core, the spread reflects the extra return investors demand to hold riskier corporate debt over safer government securities. High-yield bonds are issued by companies with lower credit ratings (below investment grade, like BB or lower), meaning they carry a higher chance of default. The spread compensates for this risk. When the spread is narrow—say, around 2.5% to 3%, as seen recently—it suggests investors are confident, willing to accept less extra yield because they perceive lower default risk or a strong economy. Narrow spreads often align with bullish markets, where cash is flowing, growth is steady, and fear is low. REF: FRED-BAMLH0A0HYM2

5I. (3/24/2025) Today’s National Average 30-Year Fixed Mortgage Rate is 6.77% (All Time High was 8.03% on 10/19/23). Last week’s data was 6.80%. This rate is the average 30-year fixed mortgage rates from several different surveys including Mortgage News Daily (daily index), Freddie Mac (weekly survey), Mortgage Bankers Association (weekly survey) and FHFA (monthly survey). REF: MortgageNewsDaily, Today’s Average Rate

The recent spike in the 30-year fixed-rate jumbo mortgage to 6.77%, compared to Freddie Mac’s rate at 6.67% and the Mortgage Bankers Association (MBA) rate at 6.93%, highlights key differences in the mortgage market. Jumbo mortgages, which exceed the conforming loan limits set by government agencies like Freddie Mac, typically carry higher interest rates because they are riskier for lenders. These loans are not backed by government entities, which increases the risk for lenders and, consequently, leads to higher rates. In contrast, Freddie Mac and MBA provide averages for conforming loans, which meet federal guidelines and have lower risk due to government backing, keeping their rates lower.

![]()

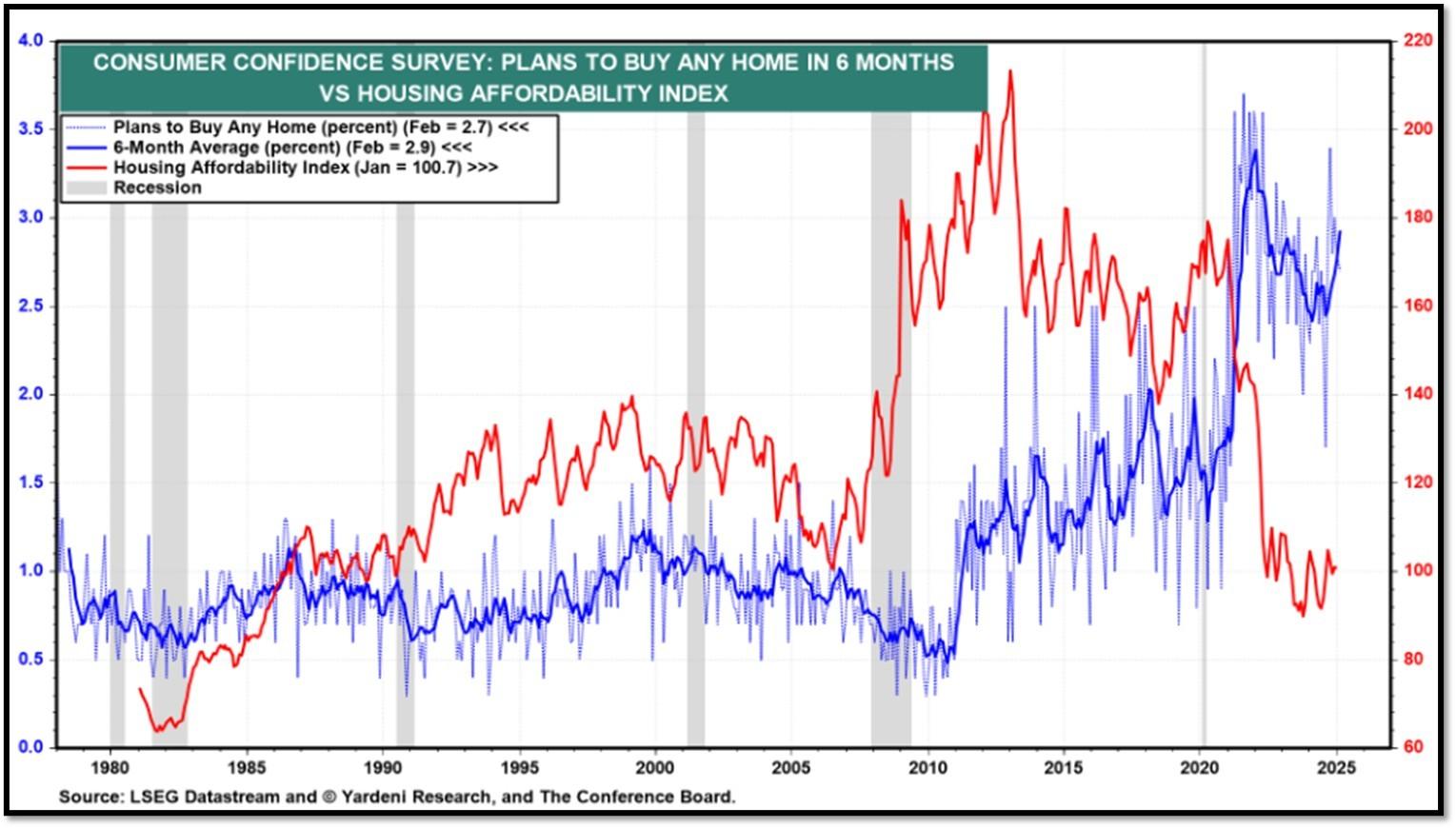

(3/17/25) Housing Affordability Index for Jan = 100.7 // Dec = 100.7 // Nov = 99 // Oct = 102.3 // Sep = 105.5 // Aug = 98.6. Data provided by Yardeni Research. REF: Yardeni

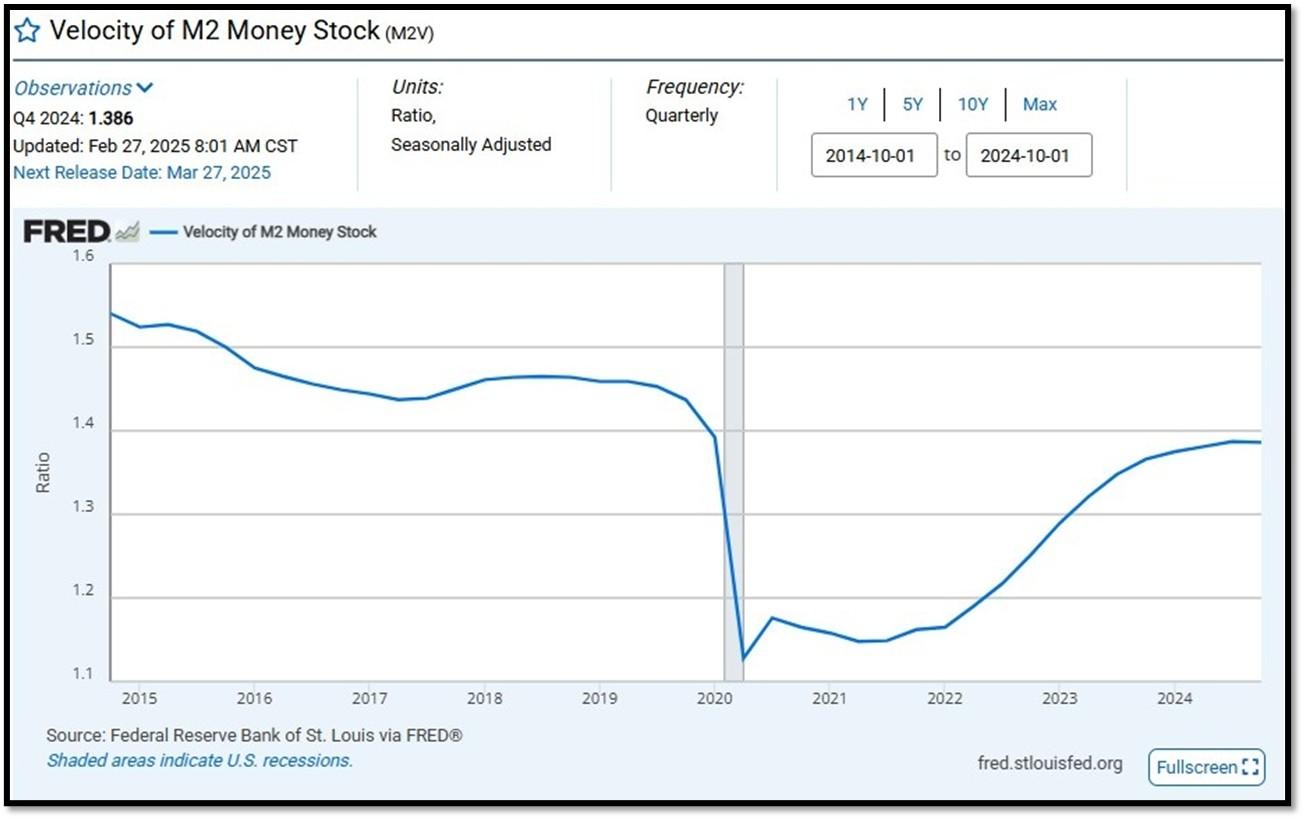

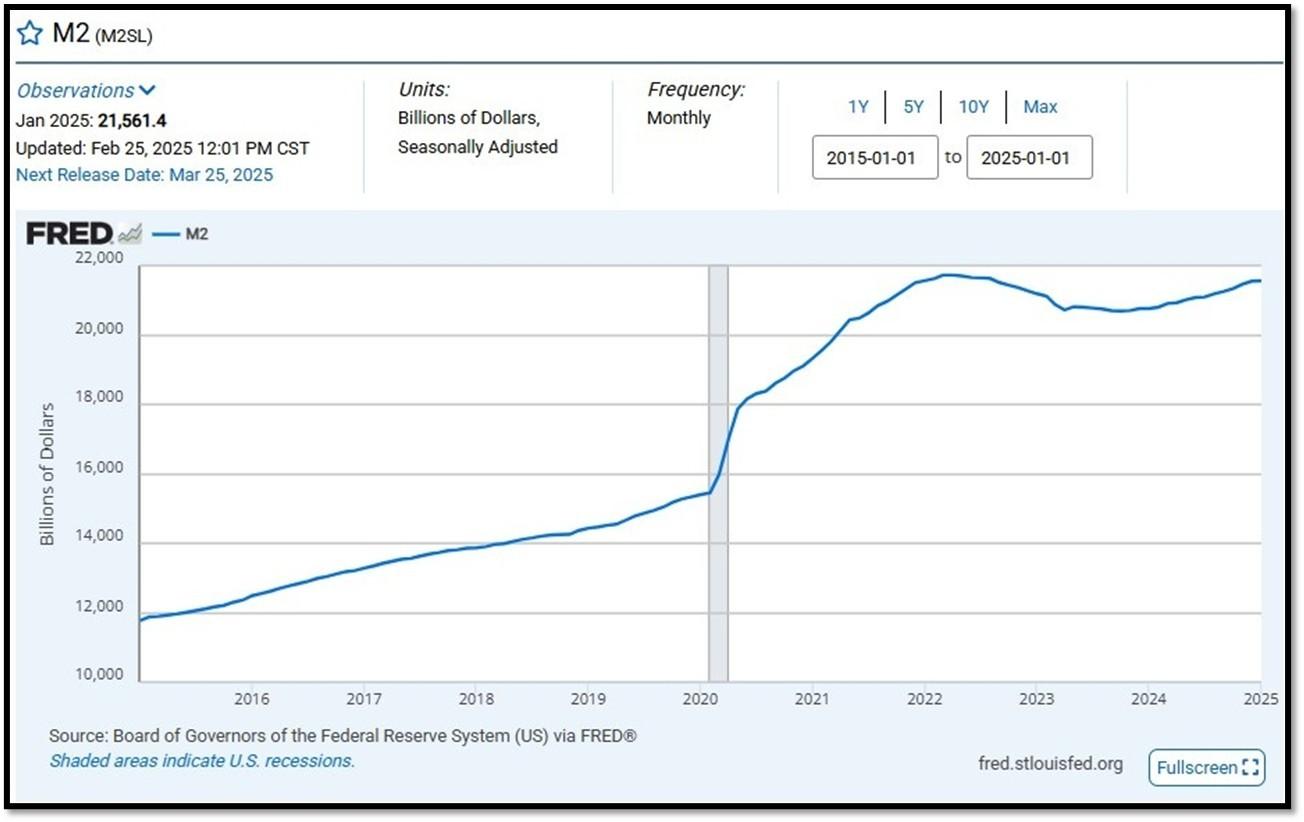

5J. Velocity of M2 Money Stock (M2V) with current read at 1.386 as of (Q4-2024 updated 2/27/2025). Previous quarter’s data was 1.390. The velocity of money is the frequency at which one unit of currency is used to purchase domestically- produced goods and services within a given time period. In other words, it is the number of times one dollar is spent to buy goods and services per unit of time. If the velocity of money is increasing, then more transactions are occurring between individuals in an economy. Current Money Stock (M2) report can be viewed in the reference link. REF: St.LouisFed-M2V

M2 consists of M1 plus (1) small-denomination time deposits (time deposits in amounts of less than $100,000) less IRA and Keogh balances at depository institutions; and (2) balances in retail MMFs less IRA and Keogh balances at MMFs. Seasonally adjusted M2 is constructed by summing savings deposits (before May 2020), small-denomination time deposits, and retail MMFs, each seasonally adjusted separately, and adding this result to seasonally adjusted M1. Board of Governors of the Federal Reserve System (US), M2 [M2SL], retrieved from FRED, Federal Reserve Bank of St. Louis; Updated on February 25, 2025. REF: St.LouisFed-M2

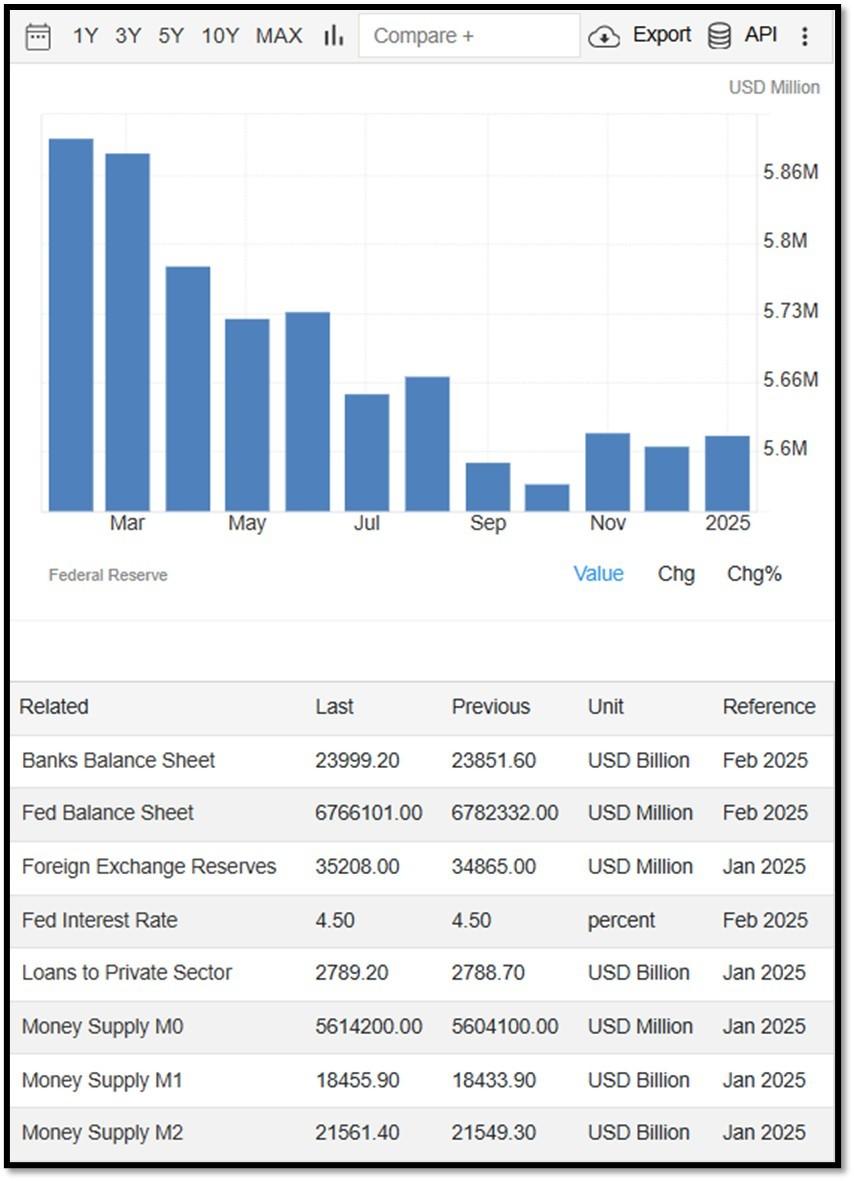

Money Supply M0 in the United States increased to 5,614,200 USD Million in January from 5,604,100 USD Million in December of 2024. Money Supply M0 in the United States averaged 1,171,888.65 USD Million from 1959 until 2025, reaching an all-time high of 6,413,100.00 USD Million in December of 2021 and a record low of 48,400.00 USD Million in February of 1961. REF: TradingEconomics, M0

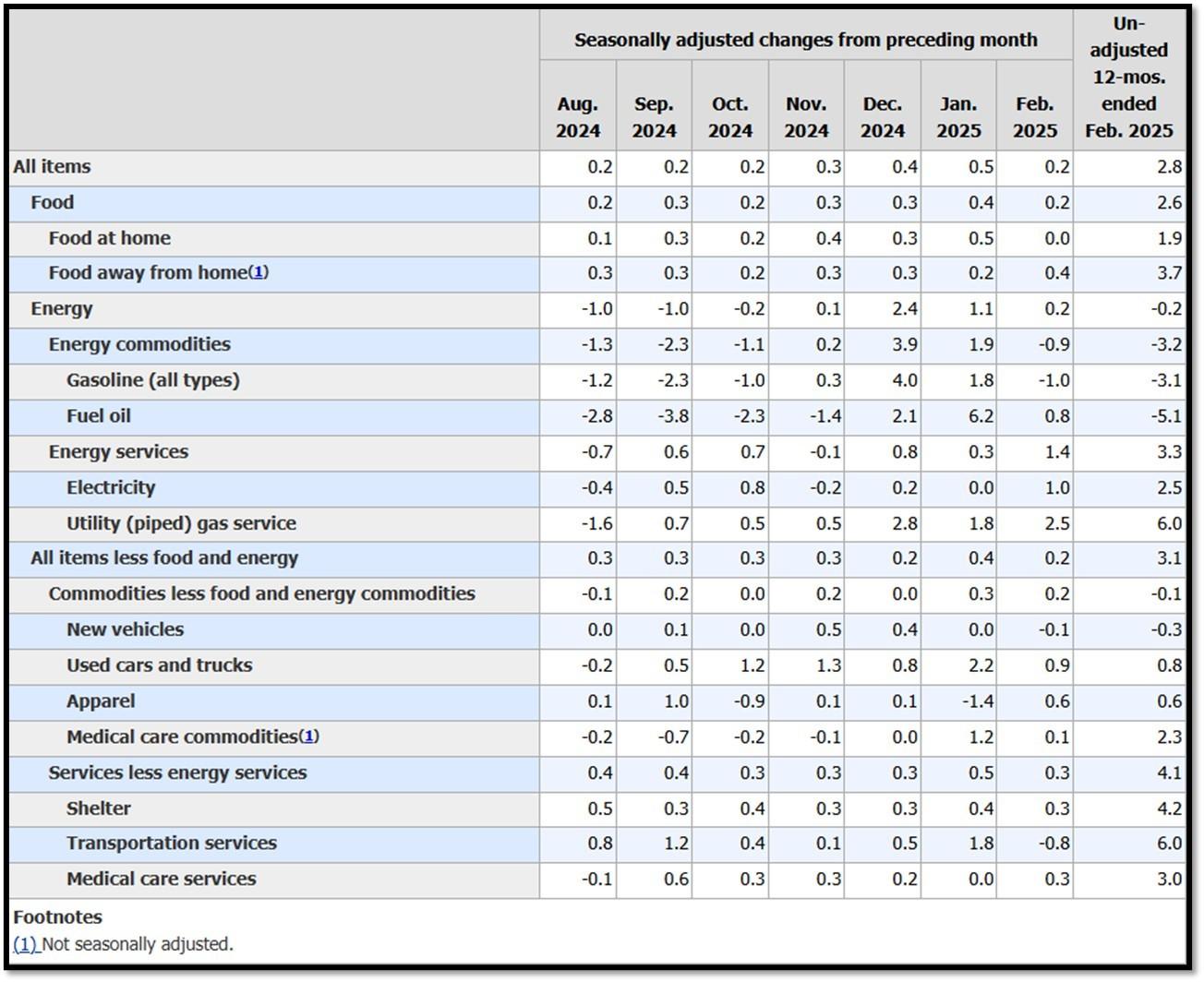

5K. In February, the Consumer Price Index for All Urban Consumers rose 0.2 percent, seasonally adjusted, and rose 2.8 percent over the last 12 months, not seasonally adjusted. The index for all items less food and energy increased 0.2 percent in February (SA); up 3.1 percent over the year (NSA). March 2025 CPI data are scheduled to be released on April 10, 2025, at 8:30AM-ET. REF: BLS, BLS.GOV

![]()

5L. Technical Analysis of the S&P500 Index. Click onto reference links below for images.

- Short-term Chart: Trend Bearish to Rising on 3/24/2025 – REF: Short-term S&P500 Chart by Marc Slavin (Click Here to Access Chart)

- Medium-term Chart: Trend Bullish to Falling on 3/24/2025 – REF: Medium-term S&P500 Chart by Marc Slavin (Click Here to Access Chart)

- Market Timing Indicators – S&P500 Index as of 3/24/2025 – REF: S&P500 Charts (7 of them) by Joanne Klein’s Top 7 (Click Here to Access Updated Charts)

- A well-defined uptrend channel shown in green with S&P500 still on up trend. REF: Stockcharts

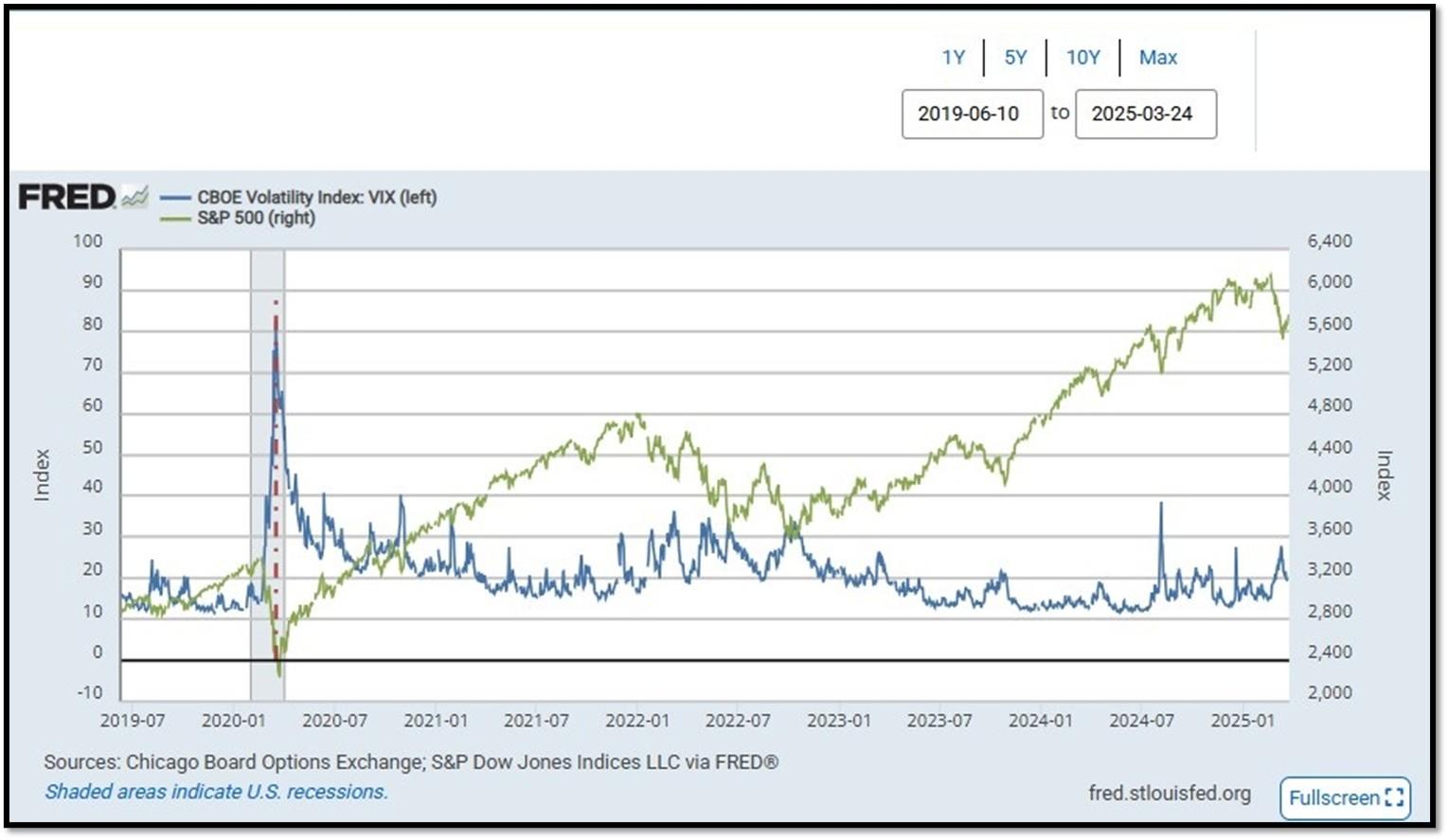

- S&P500 and CBOE Volatility Index (VIX) as of 3/24/2025. REF: FRED, Today’s Print

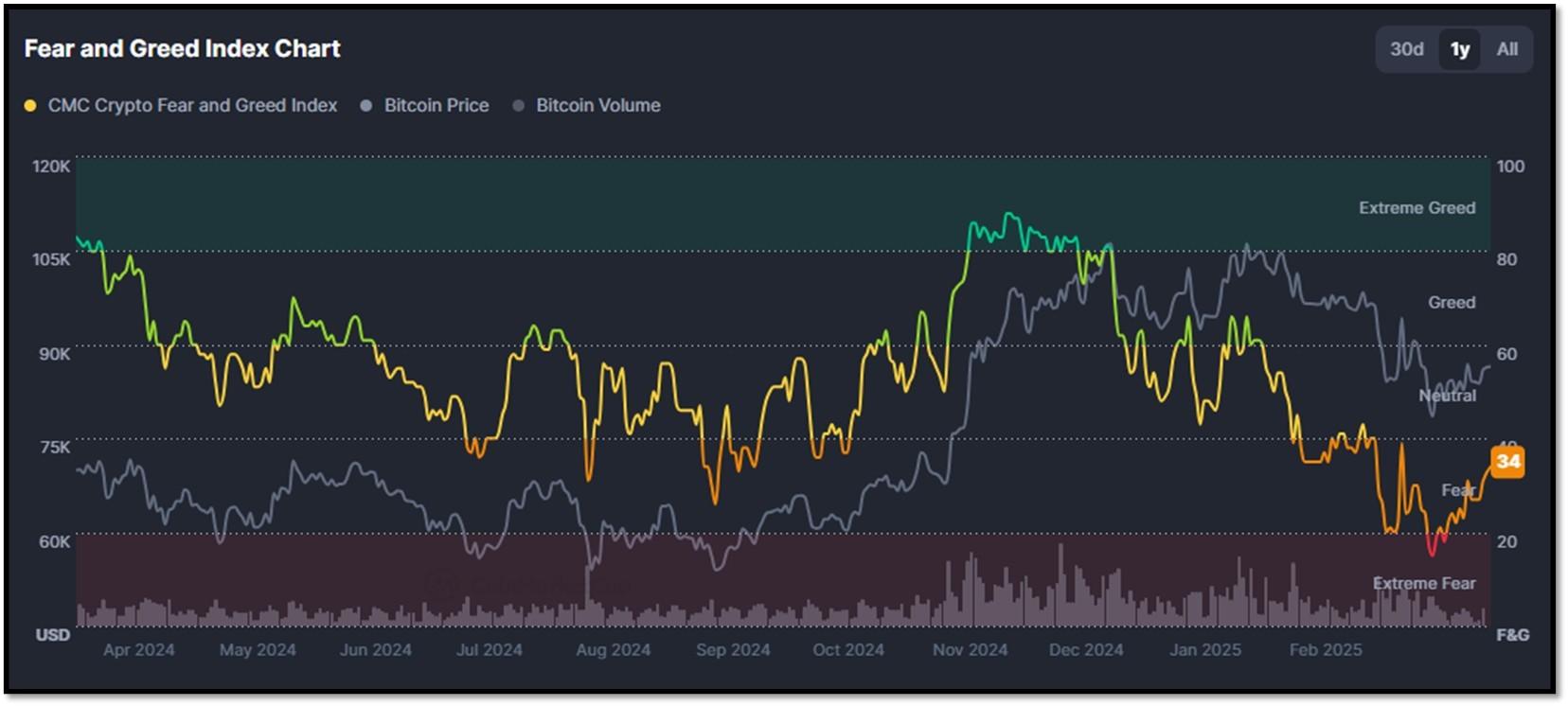

5M. Most recent read on the Crypto Fear & Greed Index with data as of 3/24/2025 is 25 (Fear). Last week’s data was 15 (Extreme Fear) (1-100). Fear & Greed Index – A Contrarian Data. The crypto market behavior is very emotional. People tend to get greedy when the market is rising which results in FOMO (Fear of missing out). Also, people often sell their coins in irrational reaction of seeing red numbers. With the Crypto Fear and Greed Index, the data try to help save investors from their own emotional overreactions. There are two simple assumptions:

- Extreme fear can be a sign that investors are too worried. That could be a buying opportunity.

- When Investors are getting too greedy, that means the market is due for a correction.

Therefore, the program for this index analyzes the current sentiment of the Bitcoin market and crunch the numbers into a simple meter from 0 to 100. Zero means “Extreme Fear”, while 100 means “Extreme Greed”. REF: Coinmarketcap.com, Today’sReading

![]()

Bitcoin – 10-Year & 2-Year Charts. REF: Stockcharts10Y, Stockcharts2Y

Len writes much of his own content, and also shares helpful content from other trusted providers like Turner Financial Group (TFG).

The material contained herein is intended as a general market commentary, solely for informational purposes and is not intended to make an offer or solicitation for the sale or purchase of any securities. Such views are subject to change at any time without notice due to changes in market or economic conditions and may not necessarily come to pass. This information is not intended as a specific offer of investment services by Dedicated Financial and Turner Financial Group, Inc.

Dedicated Financial and Turner Financial Group, Inc., do not provide tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.

Any hyperlinks in this document that connect to Web Sites maintained by third parties are provided for convenience only. Turner Financial Group, Inc. has not verified the accuracy of any information contained within the links and the provision of such links does not constitute a recommendation or endorsement of the company or the content by Dedicated Financial or Turner Financial Group, Inc. The prices/quotes/statistics referenced herein have been obtained from sources verified to be reliable for their accuracy or completeness and may be subject to change.

Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. The views and strategies described herein may not be suitable for all investors. To the extent referenced herein, real estate, hedge funds, and other private investments can present significant risks, including loss of the original amount invested. All indexes are unmanaged, and an individual cannot invest directly in an index. Index returns do not include fees or expenses.

Turner Financial Group, Inc. is an Investment Adviser registered with the United States Securities and Exchange Commission however, such registration does not imply a certain level of skill or training and no inference to the contrary should be made. Additional information about Turner Financial Group, Inc. is also available at www.adviserinfo.sec.gov. Advisory services are only offered to clients or prospective clients where Turner Financial Group, Inc. and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Turner Financial Group, Inc. unless a client service agreement is in place.